The General Directorate of Taxes (DGT), an organization dependent on the Ministry of Finance, has clarified that those over 65 years of age will not be able to benefit from the exemption in the Income Tax return for the sale of their habitual residence when they buy the house in which they had been renting for years and sell it before three years have passed since the acquisition. This is stated in the binding consultation V0278-26, of February 9, 2026, which analyzes the case of a taxpayer who had been residing as a tenant in a home that she later acquired as property and sold a year later.

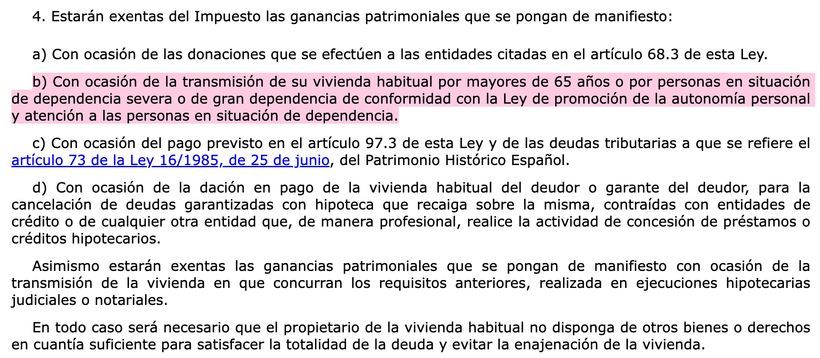

The key is in article 33.4.b) of the Personal Income Tax Law, which establishes that capital gains obtained by people over 65 years of age from the sale of their habitual residence may be exempt from tax. However, the Treasury reminds that this tax advantage requires meeting certain requirements and that the period lived in a rental regime is not taken into account to reach the minimum period required by the regulations.

CSIF mobilizes in the middle of the Income campaign: “the workforce is overwhelmed and at its limit”

The Treasury allocated 2,389 million from the Recovery Plan to pay pensions in 2024

In its response, the DGT insists that the exemption is linked not only to actually residing in the home, but also to having been the owner in full ownership of it for the legally required time.

Living for years as a rental in the home does not automatically allow the exemption to be applied

The DGT makes it clear that the fact of having lived for years in a home as a tenant does not automatically allow that home to be considered habitual for the purposes of applying the tax exemption when it is subsequently acquired and sold within three years.

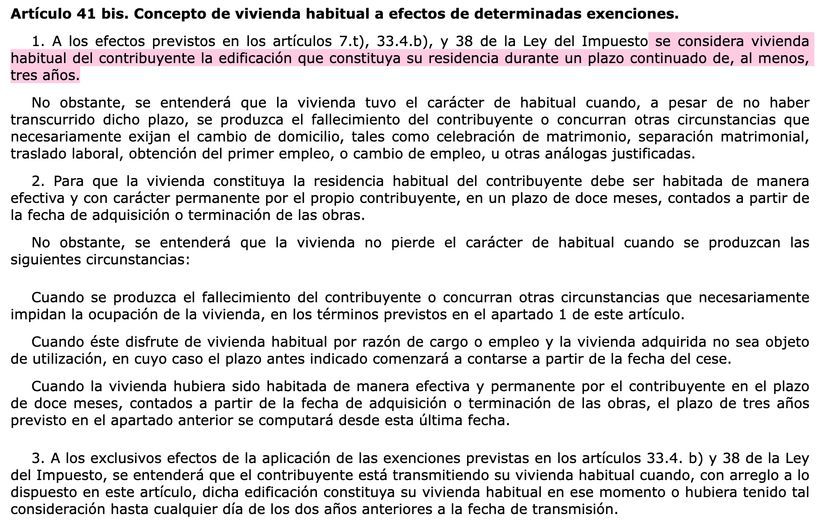

Specifically, the Treasury recalls that article 41 bis of the Personal Income Tax Regulation establishes that a habitual residence It is one in which the taxpayer has resided continuously for at least three years since its acquisition. That is, the calculation of the term begins from the moment in which ownership of the home is obtained and not from the moment when one began to live in it as a tenant.

In addition, the General Directorate of Taxes cites ruling 1858/2018 of the Supreme Court, which established doctrine on this issue. In it, the high court indicated that the application of the exemption for the sale of habitual residence for those over 65 years of age requires that the taxpayer has held full ownership of the home during those three continuous years.

In this way, the Treasury concludes that, although the taxpayer had resided in the rental home for many years, she had only been the owner for one year when she decided to sell it. Therefore, the minimum required period is not met and the home cannot be considered habitual for the purposes of applying the exemption.

The Treasury reminds that registration is not enough to prove habitual residence

Another relevant aspect of the consultation is that the DGT warns that simple registration does not in itself prove that a home is considered habitual.

In this sense, the Treasury explains that effective residence in a home is a matter of fact that must be proven by any legally valid means of proof, with its assessment corresponding to the management and inspection bodies of the Tax Agency.

Finally, the General Directorate of Taxes reminds that each case must be analyzed individually and it will be the taxpayer himself who must prove that he meets all the requirements demanded by the regulations in order to benefit from this tax advantage.