The General Directorate of Taxes (DGT), dependent on the Ministry of Finance, has clarified that having the status of young farmer is not enough to access the 100% exemption on Inheritance Tax for the transfer of an agricultural holding. This is stated in the binding consultation V0102-26, of January 20, 2026, where it analyzes the case of a 35-year-old farmer who inherited a priority agricultural holding through a legacy.

According to the DGT, although the taxpayer met the condition of young farmer and had already been recognized as a priority agricultural holding since 2019, cannot benefit from the exemption because said tax benefit requires that the acquisition occur for the farmer’s “first installation” on a priority agricultural holding.

The consultation also recalls that the acquisition of assets through inheritance or legacy constitutes a taxable event subject to Inheritance and Donation Tax in accordance with article 3.1.a) of Law 29/1987 of the ISD. Likewise, the heir or legatee is the one who must assume the payment of the tax as a taxable person.

The exemption only applies to the first agricultural installation

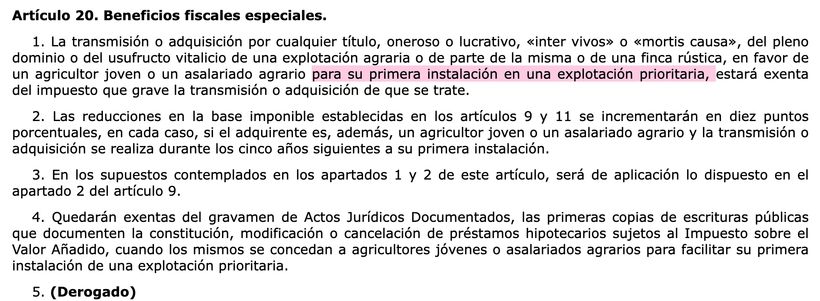

In its analysis, the DGT expressly cites article 20.1 of Law 19/1995, on the Modernization of Agricultural Holdings, which establishes a tax exemption for the transfer or acquisition of agricultural holdings, whether by inheritance, donation or sale, when carried out in favor of a young farmer or an agricultural employee for their first installation on a priority holding.

The Treasury considers that this requirement is not met in the case analyzed, since the consultant had recognized priority agricultural exploitation status since March 2019. Therefore, the inheritance received in 2025 cannot be considered a first installation.

In this way, the DGT makes it clear that access to this tax benefit does not depend only on age or status as a young farmer, but also on whether the acquisition effectively represents the beginning of the activity on a priority agricultural holding.