In Spain, workers who are approaching their ordinary retirement age wonder what amount they will receive from their retirement pension. This question is more present when it comes to salaries, for example, 1,400 euros, or when there are breaks in recent years. For Social Security, the amount of the retirement pension depends on three factors: the total number of years of contributions, the contribution bases for the latter, and the age at which the pension is accessed.

It must be taken into account that the method for calculating retirement pension has been evolving (and in fact, continues to do so) progressively since the entry into force of the Law 27/2011. For this reason, the calculation will not be the same if a worker retires in 2026 or, on the contrary, retires in 2027, since both the retirement age and the coefficients that determine the amount change each year until the reforms end, which will be this 2027.

Several retirees over 70 years old: “My father started shepherding when he was 10 or 11; he walked in the rain and wind and exchanged milk for bread.”

The Supreme Court confirms that the maternity supplement in active retirement is calculated on 100% of the pension and not on the 50% that the self-employed retiree receives

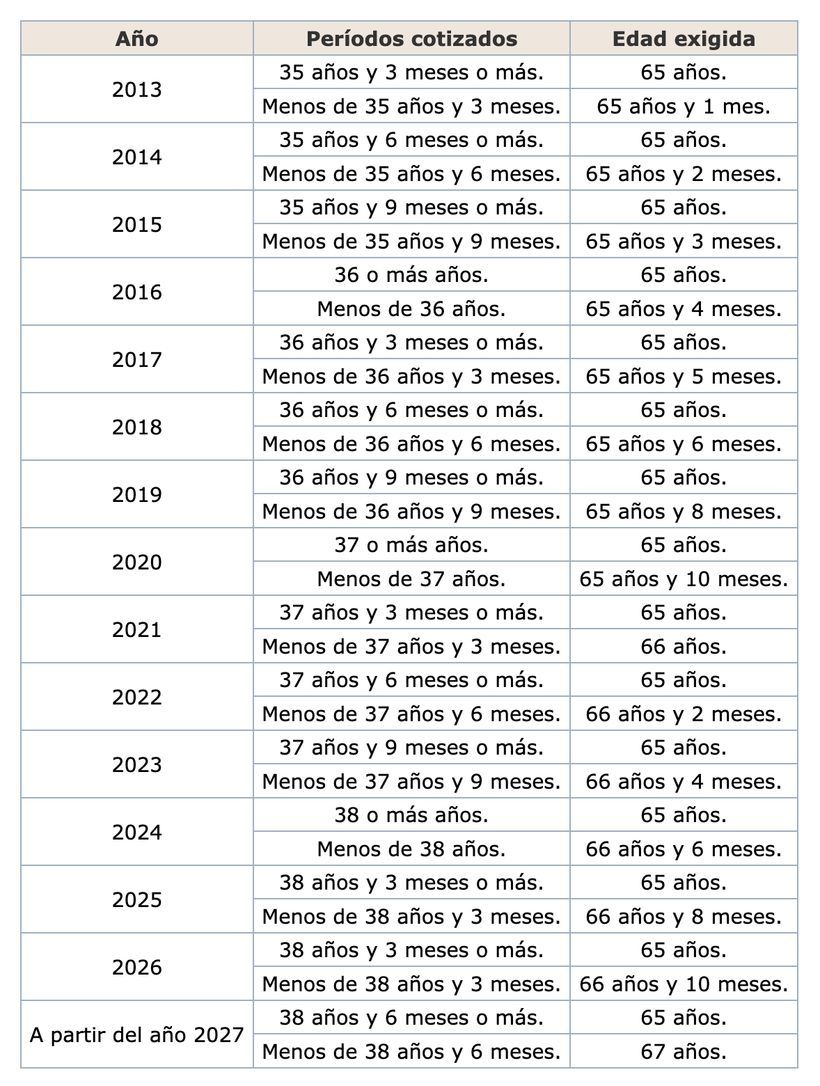

The first thing the worker must know is what year he is going to retire, information that can be consulted in the table with retirement age based on year of birth and years of contributions. For 2026, the ordinary retirement age is set at 66 years and 10 months, unless 38 years and 3 months of contributions are proven, in which case it will be 65 years. Starting in 2027, the age will be set at 67 years or 65 years when 38 years and 6 months of contributions are proven.

| Year | Quoted periods | Required age |

|---|---|---|

| 2026 | 38 years and 3 months or more. | 65 years. |

| Less than 38 years and 3 months. | 66 years and 10 months. | |

| Starting in 2027 | 38 years and 6 months or more. | 65 years. |

| Less than 38 years and 6 months. | 67 years old. |

How the retirement pension is calculated in 2026

Since January 1, 2026, two systems for calculating the regulatory base coexist and the managing entity applies ex officio the one that is most favorable to the worker, in accordance with the fourth transitional provision, section 7, of the General Social Security Law.

The current method maintains the formula in force until 2025, that is, dividing by 350 the sum of the contribution bases of the last 25 years (the 300 months prior to the month prior to the causative event).

The new method, introduced by the Royal Decree-Law 2/2023extends the calculation period and discards the worst bases. In 2026, the 302 bases with the highest amount within the previous 304 months are divided by 352.33, a scale that will grow each year until consolidated in 2037 with 324 best bases within 348 months divided by 378.

So that the oldest bases do not lose purchasing power, Social Security updates them with the CPI, except for those from the last 24 months, which are computed at nominal value. They can be consulted in the report on contribution bases from the Social Security electronic headquarters. The integration of gaps is added to the calculation, which fills the periods without contributions with fictitious contributions.

On the regulatory basis, a percentage is applied according to the years contributed. With 15 years, minimum to access the contributory retirement pension50% is recognized. From there, each of the following 49 months adds an additional 0.21%, and each of the subsequent 209 months, an extra 0.19%.

In this way, 36 years and 6 months of contributions give the right to 100% of the regulatory base. These coefficients are valid until December 31, 2026: in 2027 they will change and it will take 37 years of contributions to reach 100%, according to the ninth transitional provision of the LGSS.

What happens if the contribution base is not equal to my salary

It must be clear that, as we have seen, the calculation of the pension is carried out on the contribution bases and not on the worker’s net salary. A gross salary appears on the payroll, which serves as a reference to set the contribution base. Deductions (the worker’s contributions and personal income tax withholdings) are subtracted from this gross amount to obtain the net salary.

The base may be different from the salary, but it can never be less than the minimum contribution base. For this year 2026, according to the Order PJC/297/2026, of March 30the minimum contribution base of the General Regime is set at 1,424.40 euros per month (although it may vary depending on the group).

How much pension is left with a salary of 1,400 euros

People who receive a gross salary of 1,400 euros per month should know that their company will contribute for the legal minimum base, since the salary is slightly below the threshold set for 2026. Taking this minimum base of 1,424.40 euros as a reference and applying the regulatory base formula, the result is 1,220.91 euros (1,424.40 euros × 300 months / 350).

The corresponding percentage will be applied to this amount based on the years of contributions, which places the pension between 610.46 euros per month with 15 years of contributions and 1,220.91 euros per month with 36 years and 6 months of contributions (provided that the minimum supplement is not applicable).

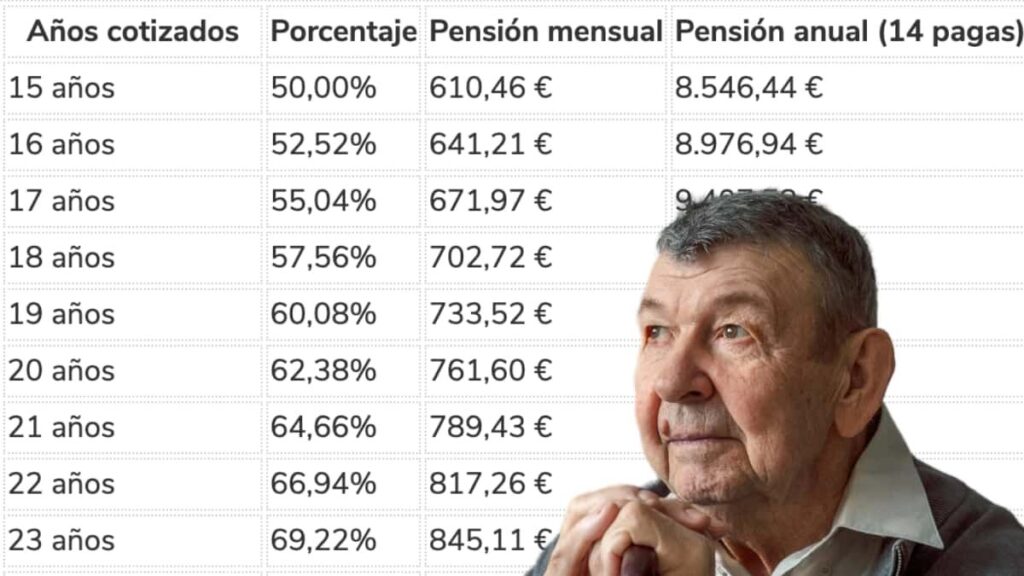

In the following table, as a guide, you can consult the pension that would correspond to a salary of 1,400 euros depending on the years of contributions. It does not apply the effect of inflation on the oldest bases, nor the integration of gaps, nor the supplement to minimums to reach the minimum pension amounts.

| Years quoted | Percentage | Monthly pension | Annual pension (14 payments) |

|---|---|---|---|

| 15 years | 50.00% | €610.46 | €8,546.44 |

| 16 years | 52.52% | €641.21 | €8,976.94 |

| 17 years | 55.04% | €671.97 | €9,407.58 |

| 18 years | 57.56% | €702.72 | €9,838.08 |

| 19 years | 60.08% | €733.52 | €10,269.28 |

| 20 years | 62.38% | €761.60 | €10,662.40 |

| 21 years | 64.66% | €789.43 | €11,052.02 |

| 22 years | 66.94% | €817.26 | €11,441.64 |

| 23 years | 69.22% | €845.11 | €11,831.54 |

| 24 years | 71.50% | €872.94 | €12,221.16 |

| 25 years | 73.78% | €900.79 | €12,611.06 |

| 26 years | 76.06% | €928.62 | €13,000.68 |

| 27 years | 78.34% | €956.46 | €13,390.44 |

| 28 years | 80.62% | €984.30 | €13,780.20 |

| 29 years | 82.90% | €1,012.13 | €14,169.82 |

| 30 years | 85.18% | €1,039.97 | €14,559.58 |

| 31 years | 87.46% | €1,067.80 | €14,949.20 |

| 32 years | 89.74% | €1,095.64 | €15,338.96 |

| 33 years | 92.02% | €1,123.49 | €15,728.86 |

| 34 years | 94.30% | €1,151.32 | €16,118.48 |

| 35 years | 96.58% | €1,179.16 | €16,508.24 |

| 36 years | 98.86% | €1,207.01 | €16,898.14 |

| 36 years and 6 months | 100.00% | €1,220.91 | €17,092.74 |