Spain has been reforming its pension system for more than 15 years in the face of the inexorable demographic winter (more longevity, more aging and retirement of the “baby boom”). From Law 27/2011, which introduced the calculation method and the two retirement ages, to Decree Law 2/2023 with a dual system and the MEI, the Government’s objective was and is to make our system sustainable and viable. But, if we look at the international map, we see how the master class in financial survival does not come from the parametric adjustments of southern Europe, but from the North Atlantic. Iceland has positioned itself as the most resilient pension system on the planet in the face of budgetary pressure and population aging.

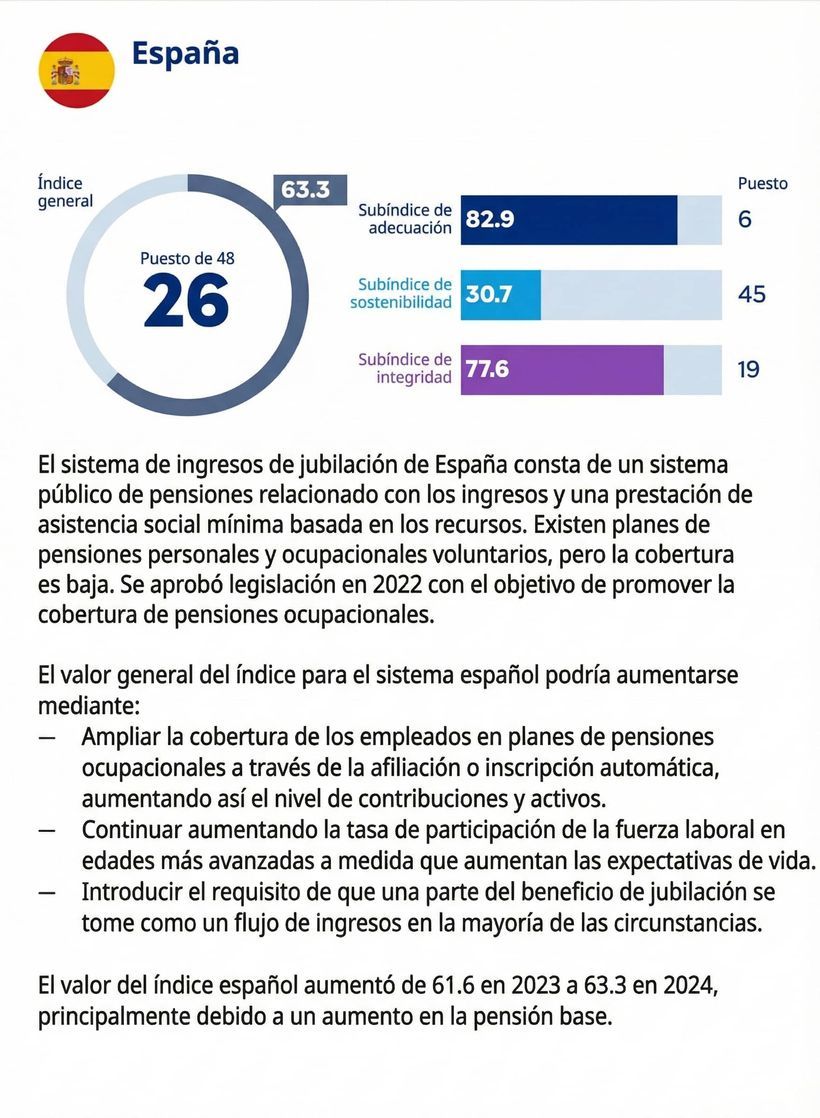

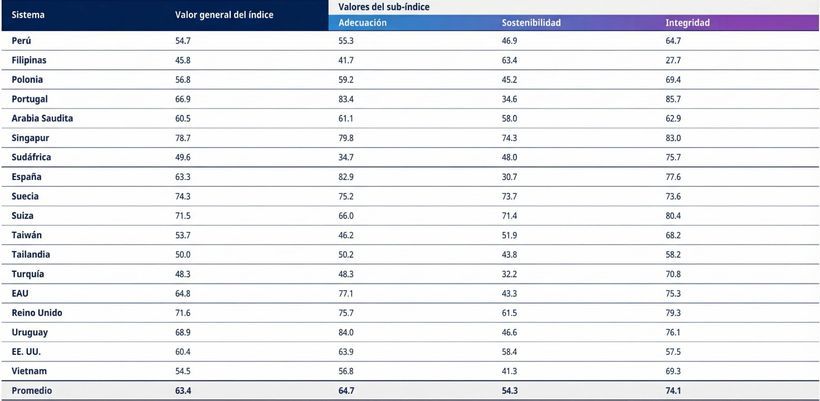

According to the study of Mercer CFA Institute Global Pension Index 2025Iceland is the second best system in the world with an overall score of 84.0 (Rating A) and holds the absolute number one in the “sustainability” subindex with a score of 85.7. Spain, for its part, lags behind in the C+ category with 63.8 overall points, weighed down by an alarming fragility in its ability to endure over time (34.2 in sustainability).

The comparison is uncomfortable for the Spanish model because the international ranking does not penalize the generosity of payments. In fact, both countries are virtually tied in their current ability to financially protect their retirees (with an adequacy score of 83.0). The abysmal difference lies in how they finance that long-term promise.

Unlike Spain, Iceland has a capitalization mechanism for all citizens. By law, every Icelandic worker between 16 and 70 years old has a mandatory minimum contribution to pension funds amounting to 15.5% of their salary. Of this fee, 4% is contributed directly by the employee and 11.5% is borne by the employer. That is, something similar to our “Intergenerational Equity Mechanism”, but with the difference that what is contributed goes to the future retiree and not to pay current pensions.

This constant injection of capital nourishes a mixed system that does not depend exclusively on the current year’s tax collection. Through these mandatory capitalization occupational plans, together with a state pension that guarantees a base of 365,592 Icelandic crowns per month (about 2,560 euros at the exchange rate), the system is immunized against demographic swings.

In contrast, Spain trusts its future to a pure pay-as-you-go system. Recent reforms, such as the Intergenerational Equity Mechanism (MEI), seek to alleviate tension by raising the contribution by 0.90% in 2026 (0.75% paid by the company and 0.15% by the worker), but the money is used to pay current pensions and provide a liquidity reserve fund, without generating real and individualized wealth in the long term.

Delay the retirement age to 67 years

The viability of the Icelandic model is also supported by exceptional labor participation at older ages. While the ordinary retirement age in Spain is 66 years and 10 months in 2026 (with a view to 67 years in 2027), Iceland has already established its normal barrier at 67 years.

Beyond the norm, Iceland stands out greatly for its culture of retaining senior talent, operating with one of the highest activity and employment rates in Europe, which reduces the average years of collection of pensioners and relieves pressure on younger generations.

In the analysis of the best-rated systems, experts emphasize that the key to sustainability lies precisely in “increasing the state retirement age and promoting greater participation in the workforce at older ages.”

The warning for the future Spanish model

Why does Iceland get the praise and Spain the warnings? The CFA Institute defines “A” grade systems as those that constitute “a robust retirement income system that offers good benefits, is sustainable and has a high level of integrity.” Spain scores well in the immediate protection factor, but fails miserably in the foundations that ensure that the accounts balance when the generation of the baby boom finish retiring.

Europe is moving inexorably towards mixed ecosystems where responsibility is shared. Policies that limit all efforts to increasing the tax burden on companies and public debt show signs of exhaustion. Iceland’s lesson for Spain is that protecting purchasing power is laudable, but without an institutional architecture that drives large-scale mandatory private savings and a labor market designed to retain senior talent, the promise of pensions is built on unsustainable demographic terrain.