Advancing the retirement age implies accepting that Social Security applies reducing coefficients that reduce the pension forever, that is, a percentage that is discounted for each month advanced with respect to the ordinary age and that can reach 30%. Many pensioners assume that this cut will also drag down the pension that their spouse will receive when they die, and that paralyzes decisions that were already made. Alfonso Muñoz Cuenca, a Social Security official specialized in pensions and benefits, has published a video on his channel where he explains that widowhood is calculated on the regulatory basis of the deceased, not on the already reduced pension that he had been receiving during his lifetime.

This issue matters a lot, since according to the latest data from Social Security, in Spain about 2.3 million people receive a widow’s pension, of which 95% are women. And a significant part of the pensioners who generate them retired before their ordinary age, which multiplies the consultations with advisors and officials about how this cut is transferred to the survivor.

Social Security penalizes the pension of those who decide to retire early, but this cut will not affect their spouse’s future widow’s pension.

The Supreme Court denies a widow’s pension to a woman after 22 years of cohabitation and two children together: she did not register as a de facto couple

How widowhood is calculated when the deceased was a pensioner

“The widow’s pension is calculated on the same regulatory basis that was used to calculate the retirement pension, not on the amount that the pensioner is currently receiving,” explains Muñoz. The regulatory base is the theoretical figure that results from averaging the worker’s contribution bases during a specific period before retiring. To understand it better, it is the starting number with which the system calculates any contributory pension, regardless of subsequent adjustments.

On that basis, a general percentage of 52% is applied, which can rise to 60% for people over 65 years of age with no other income and up to 70% when the beneficiary has family responsibilities and the pension is their main source of income. The regulation is included in articles 219 to 223 of the consolidated text of the General Law of Social Security and developed by Royal Decree 1647/1997 and the subsequent regulations that establish the current percentages.

When the deceased was already a pensioner, the rule considers him or her the person responsible for the benefit and does not require the heirs to prove additional periods. Muñoz specifies it as follows: “In this case, the law considers the deceased pensioner to be the cause and no minimum additional contribution period is required.” The spouse will only have to prove the bond and the cohabitation or de facto partnership requirements established by Social Security itself.

The numerical example that dispels the doubt

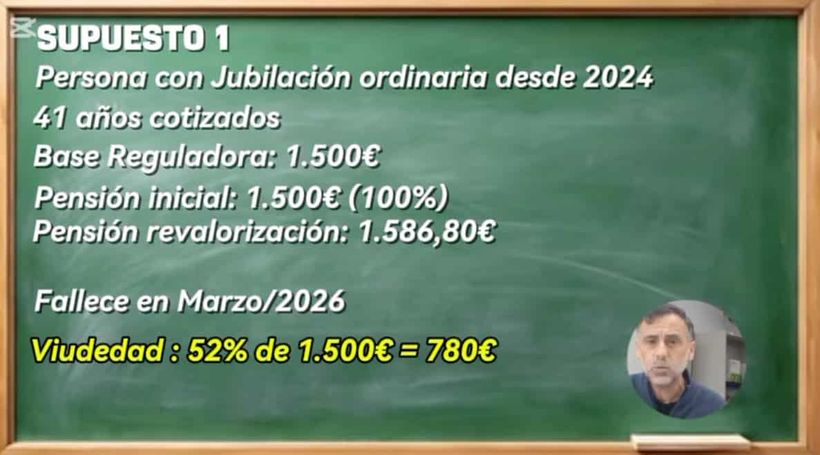

To make it clearer, the official puts two parallel scenarios with equivalent figures. In the first, a worker with 41 years of contributions and a regulatory base of 1,500 euros retires at the ordinary age with the right to 100% of the pension. After two consecutive revaluations, he ends up earning 1,586.80 euros per month. If you die, your spouse receives 52% of the 1,500 euros base, which amounts to 780 initial euros and, once the revaluations from the causative event (the moment the retirement was recognized) have been applied, 823.49 euros per month.

In the second scenario, the same person with the same 41 years of contributions retires one year before his or her ordinary age. The regulatory base remains identical, 1,500 euros, but when a reducing coefficient of 5.25% is applied for anticipation, your initial pension drops to 1,421.25 euros. Here the reader’s logical question arises: does widowhood also decrease? “Well no. The widow’s pension is recalculated on the regulatory basis of 1,500 euros, not on the reduced pension that the pensioner received,” Muñoz responds. The result for the spouse is exactly the same, 823.49 euros per month.

What requirements does Social Security require from the deceased?

Alfonso takes advantage of the video to review the cases in which the system recognizes the pension. If the deceased was an active worker, Social Security requires that he or she be registered or in an equivalent situation and that he or she had contributed at least 500 days within the five years prior to death. If you were not registered at the time of death, the bar rises to 15 years of contributions throughout your entire working life.

When the death is due to an accident, whether work-related or not, or an occupational disease, “no prior contribution period will be required,” recalls Muñoz. And if the deceased was already a retirement or permanent disability pensioner, the system considers the contribution requirement fulfilled with the pension he/she was receiving, without requesting additional contributions.

The surviving spouse, the de facto couple registered with the advance notice required by law and the ex-spouse who received compensatory pension may be beneficiaries, provided that the general requirements are met. The pension is also compatible with the beneficiary’s own retirement or permanent disability pension and with income from work, a key difference compared to other benefits in the system.

To finish, the Social Security official makes a summary to have a clear idea and that is that “the widow’s pension is calculated on the regulatory basis of the deceased pensioner, not on the reduced amount that he had been receiving as a consequence of early retirement.” That is, early retirement penalizes the pensioner, but not the surviving spouse.