Public pension systems in Europe are based on the same principle, pay-as-you-go. The contributions of current workers finance the income of current retirees, a mechanism that guarantees intergenerational solidarity, universal coverage and the stability of Social Security. Countries such as the Netherlands, Iceland and Denmark are often considered role models for their sustainability and performance.

However, when you look outside the continent, other leading references come into view. This is the case of Singapore and its Central Provident Fund (CPF), which stands out as one of the strongest retirement guarantees in the world. Although at first glance it works in a similar way through mandatory contributions from workers and employers, its design is very different from that of European pensions.

You may be interested

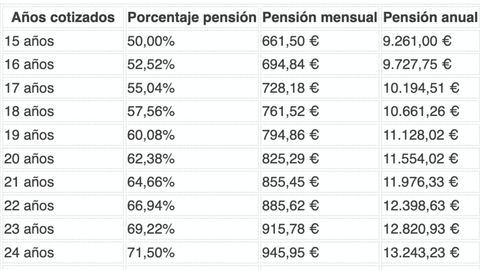

Table with the retirement pension that you will have according to the years of contributions if you receive the Minimum Interprofessional Wage

Social Security denies raising the retirement age to 70 years and guarantees the future of pensions

So what sets the CPF apart from the rest? These are the 5 keys to understanding its singularities that differentiate it from the Spanish model, as explained by the government itself in its Web page.

A 3 in 1 system

European plans, including the Spanish one, allocate workers’ contributions to finance future retirement income. However, Singaporeans’ CPF provides three savings avenues within a single tool that are divided into separate accounts:

- Ordinary Account (OA): for the purchase of housing, education and insurance.

- Special Account (SA): only and exclusively for when the worker retires.

- MediSave: for medical expenses.

In Spain, Social Security contributions are not used for other social issues such as housing and health.

High and guaranteed returns

The CPF offers a risk-free interest that can reach 6% annually for those over 55 years of age and 5% for minors, with a minimum of 4% guaranteed in accounts intended for retirement and health.

In Spain, contributions do not generate individual financial returns, they only serve to calculate a future public pension. The growth of the “fund” in Singapore does not depend on the markets, but on a state guarantee, which is why it is one of the most stable systems in the world.

The basis of its sustainability is that each remuneration depends on what has been accumulated

In Singapore, the amount each person receives upon retirement depends on their actual savings, not the country’s taxes and demographics. Members must reach the Basic Retirement Amount (CBR) which is calculated according to the actual expenses of pensioners’ households.

If a citizen wants to increase their future subsidy they have two options: they can top up the CPF or they can postpone the start of collection.

Unlike the CPF, many others, such as the Spanish one, are financed by taxpayers’ taxes. Due to the rapid aging of the population and the few young people contributing, it is subject to enormous financial pressure that forces remuneration to be reduced or the retirement age to be delayed, implying serious harm to the beneficiaries.

Contributed by the worker, employers, family members and the State

In addition to the 20% that the worker contributes to the CPF, individual efforts are complemented by contributions from employers and contributions from family members and the State itself with additional income.

Income in Spain depends exclusively on the years of contributions and the contribution bases of each worker. The options detailed above do not exist.

Savings are not lost upon death, they are inherited by the beneficiaries

Most funded pension systems are discontinued when the person dies, however, unused CPF funds are distributed to beneficiaries or family members.

Singapore’s is complemented by other government programs to reinforce social coverage:

- ComCare Long-Term Assistance: This is a monthly benefit for people who cannot work regularly as a result of old age and/or illness, and who have little or no family support.

- Lease Buyback Scheme: In Singapore, most public housing flats owned by the Housing & Development Board (HDB) are not bought outright, but on a 99-year lease. This plan allows older people to “sell” part of the remaining years of their apartment lease to the HBD and thus receive money in exchange for their CPF retirement account, in addition to being able to continue living in their home.

- Matching Retirement Savings Plan: Provides a dollar-for-dollar match for additional contributions to the fund by senior Singaporeans with lower CPF balances.

- Senior Housing Bonus: Provides senior households in Singapore with a cash bonus when they move into a flat with 3 bedrooms or less, which will be used to supplement their CPF Retirement Account and join CPF LIFE.

- Aged Support Scheme: This is a quarterly cash payment to Singaporeans aged 65 and over who have had low incomes throughout their lives and now have little or no family support.

- Earned Income Supplement: Provides cash payments and additional CPF contributions to lower-paid Singaporean workers.