Although many people think that “giving up an inheritance” is a simple way to avoid debt or problems, the reality is more complex. This waiver cannot be made at any time without tax consequences, since it must be done before the tax expires. Now, can you renounce an inheritance after, for example, ten years? The answer is that “legally yes, but fiscally it is a disaster.” If you do so, the Treasury will treat you as “if you had first accepted the inheritance and then donated it.”

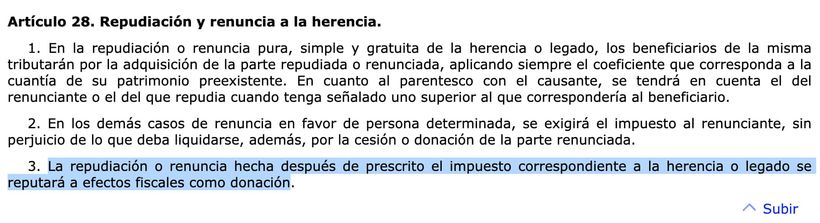

This is so, since article 28.3 of the Inheritance and Donation Tax Law (consultable in this BOE) explains that “the repudiation or renunciation made after the tax corresponding to the inheritance or legacy has expired will be considered a donation for tax purposes.” Thus, the statute of limitations for the tax is, generally, four years (As stated in article 66 of the General Tax Law). Therefore, the law understands that if you let that time pass without renouncing (or paying the tax), you have “tacitly” accepted the inheritance.

You may be interested

The Treasury confirms that two retirees must pay 48,956.59 euros of personal income tax on their two pensions and justice forces them to be forgiven since they are exempt

Justice forces the Treasury to return 7,496.91 euros from the income tax return to a KLM employee who worked from Holland and was exempt from personal income tax

Just as the Law says, resigning late is not resigning, at least in the eyes of the Administration, since what has happened is that the heir, by allowing the tax to expire, has consolidated his right over the assets (he has inherited) and, immediately afterwards, has decided to “donate” those same assets to the next in line of succession.

In this way, the amount of the inheritance does not matter, if the renunciation is not made in a timely manner, the Treasury does not consider it a “repudiation”, but rather a “lucrative transfer” or donation.

The tax consequences of resigning “late”

What does this mean in practice? If an heir renounces before the statute of limitations (“pure, simple and gratuitous renouncement”), it is understood that he has never possessed the assets. The inheritance “jumps” to the next heir (for example, from the son to the grandson), who will be taxed by Inheritance as if he inherited directly from the original deceased, that is, if it were only a single tax operation.

Now, if the renunciation is made after the statute of limitations, the law treats it as a donation. In this scenario, the heir who renounces “late” becomes a donor, and the person who receives those assets (the “beneficiary” of the renouncement) becomes a donee.

In this case, that person will have to pay the Donation Tax, which is usually much more expensive and has fewer bonuses than the Inheritance Tax. Now, you must know that evading this rule due to ignorance is very common and ends up costing a lot of money in taxes.

A case study on a prescribed waiver

To understand it better, let’s take this practical example, in which Juan’s father dies, leaving him an apartment as an inheritance. Juan does not do any paperwork. Six years pass, and when he wants to sell the apartment, he discovers that it is not in his name. He then decides to go to the notary and “give up” the inheritance so that it passes directly to his own daughter (the granddaughter of the deceased), thinking that this way he will save himself a step.

The problem is that the Inheritance Tax on his father’s inheritance has already expired. By making the resignation “late”, article 28.3 is activated. The Treasury considers that Juan tacitly accepted the apartment six years ago and that he is now donating it to his daughter. Juan’s daughter will not pay the Inheritance Tax (which could be subsidized), but will have to pay a Donation Tax for the value of the apartment. An error that duplicates the tax bill.

What happens if the resignation is made on time?

In the opposite case, if Juan had gone to the notary within the legal deadlines (before the statute of limitations) to make a “pure, simple and free repudiation”, the scenario would be totally different. Legally, Juan would never have been an heir.

According to the law, this resignation “on time” would have caused the inheritance of the apartment to pass directly to his daughter (the granddaughter), who would have settled the Inheritance Tax taking into account the relationship with her grandfather. Its purpose is to protect the right to resign, but it must always be done respecting the deadlines established by law to prevent an act of resignation from becoming, in the eyes of the Treasury, a generous (and expensive) gift.