The amount of the retirement pension depends, according to the National Social Security Institute (INSS), on the total number of years of contributions and the contribution bases for the last 25 years. In the case of workers who receive the Minimum Interprofessional Wage (SMI), although they are entitled to 100% of the pension, the final amount could be lower. This happens because their contribution base is small, so many ask themselves: What pension would I have if I collected the SMI based on the years worked?

Right now, the minimum wage is set at 1,184 euros per month in 14 payments or 1,381.33 euros gross with the 2 extraordinary payments prorated. That is, in total there are 16,576 gross annual euros. Now, to calculate the amount of the retirement pension, it must be taken into account that Social Security does not take the gross or net salary, but rather the contribution bases. In other words, the contribution base will be used to calculate the regulatory base or 100% of the pension to which one may be entitled based on the years of contributions.

You may be interested

Kathy (81 years old): “I can’t retire, so I work part-time. When I finished high school, women couldn’t do everything I wanted, so I never amounted to anything”

Social Security denies raising the retirement age to 70 years and guarantees the future of pensions

Of course, as long as you know that to access the contributory pension you must have a minimum of 15 years of contributions, of which at least two must be within the last 15 years. On the other hand, meeting the ordinary age, which we remember for 2026, will be set at 66 years and 10 months unless you have a total of 38 years and three months of contributions, which can be retired at age 65.

How the pension is calculated if you earn the minimum wage

To calculate the pension, it is first necessary to determine the regulatory base, which represents 100% of the theoretical pension to which one is entitled. Its calculation is based on the contribution and not on the net salary received. Those people who receive the Minimum Interprofessional Salary (SMI) must have the minimum contribution base, which has been set for 2025 at 1,381.20 euros per month, according to Order PJC/178/2025.

The regulatory base is obtained by dividing the contribution bases of the last 300 months (25 years) by 350. Keep in mind that if there are periods without contributions, the gap integration rules will be applied, that is, the first 48 empty monthly payments are counted for 100% of the current minimum base, and the remaining ones for 50% of said base. In addition, Social Security applies a coefficient to update the oldest bases according to inflation (CPI).

Once the regulatory base is obtained, the final percentage of the pension depends on the years worked. With 15 years of contributions (the minimum required) you are entitled to 50% of the base. From there and according to the regulations in force until 2026, 0.21% is added for each of the next 49 months, and 0.19% for the subsequent 209 months.

In this way, to collect 100% in the period in 2026, 36 years and six months of contributions are necessary, but knowing that from 2027, 37 years will be necessary.

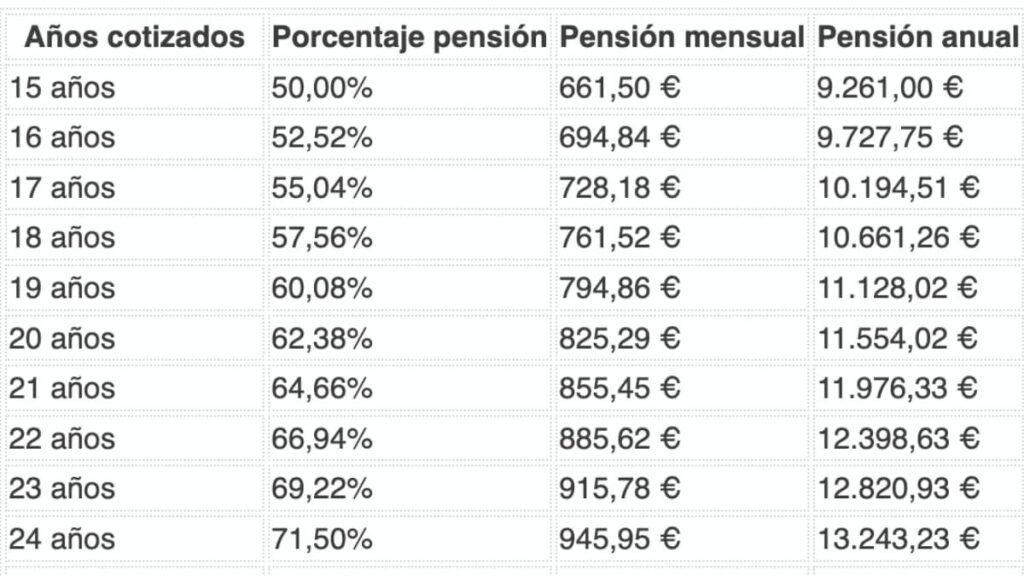

Table to calculate your pension according to the years of contributions if you earn the minimum wage

Assuming that we always quoted for the current minimum base, the resulting regulatory base would be 1,183.89 euros (result of applying the formula: 1,381.20 x 300 / 350). This amount represents 100% of the pension to which we would be entitled if we complete the required years; Otherwise, the pension will be reduced by applying the corresponding percentage. In the following table you can see, as a guide, what pension would remain according to the years of contributions.

| Years quoted | Pension percentage | Monthly pension (x14) | Annual pension |

|---|---|---|---|

| 15 years | 50.00% | €690.60 | €9,668.40 |

| 16 years | 52.52% | €725.41 | €10,155.74 |

| 17 years | 55.04% | €760.21 | €10,642.94 |

| 18 years | 57.56% | €795.02 | €11,130.28 |

| 19 years | 60.08% | €829.82 | €11,617.48 |

| 20 years | 62.38% | €861.59 | €12,062.26 |

| 21 years | 64.66% | €893.08 | €12,503.12 |

| 22 years | 66.94% | €924.58 | €12,944.12 |

| 23 years | 69.22% | €956.07 | €13,384.98 |

| 24 years | 71.50% | €987.56 | €13,825.84 |

| 25 years | 73.78% | €1,019.05 | €14,266.70 |

| 26 years | 76.06% | €1,050.54 | €14,707.56 |

| 27 years | 78.34% | €1,082.03 | €15,148.42 |

| 28 years | 80.62% | €1,113.52 | €15,589.28 |

| 29 years | 82.90% | €1,145.01 | €16,030.14 |

| 30 years | 85.18% | €1,176.51 | €16,471.14 |

| 31 years | 87.46% | €1,208.00 | €16,912.00 |

| 32 years | 89.74% | €1,239.49 | €17,352.86 |

| 33 years | 92.02% | €1,270.98 | €17,793.72 |

| 34 years | 94.30% | €1,302.47 | €18,234.58 |

| 35 years | 96.58% | €1,333.96 | €18,675.44 |

| 36 years | 98.86% | €1,365.45 | €19,116.30 |

| 36 years and 6 months | 100.00% | €1,381.20 | €19,336.80 |

As you can see, depending on the years the amount could be below the current minimum pension. In this sense, if the pension falls below the minimum amount that corresponds to the family situation (these are the minimum amounts for 2025), it can be completed up to that amount with the application of the minimum supplement.