In 2026, the method of calculating retirement pensions will change again, since the new dual system will enter and for this reason, almost all workers want to know what pension they will have depending on the years of contributions. When determining the amount, the National Social Security Institute takes into account the contribution bases of recent years and the total number of years worked. That is, the more years worked and the greater the contribution base, the higher the pension will be.

Although the method for calculating the retirement pension is regulated in Law 27/2011, which will be maintained until 2027, the second pension reform, known as “the Escrivá Law” under the Royal Decree 2/2023established a new dual calculation system.

You may be interested

Arrate Aranceta (79 years old), widowed since she was 40 years old and with 4 children, speaks clearly about her pension: “It was 400 euros to pay for food and studies, it was not enough”

Several retirees over 80 years of age speak clearly: “I regret having given my properties to my daughters prematurely. They sold what I wanted.”

Until now, the regulatory base, which is so to speak 100% of the pension to which one is entitled according to the years of contributions, was calculated based on the last 300 contribution bases (which are 25 years) and the result by dividing it by 350 (this is so, since the bases are for 12 payments and the pension for 14). What was happening with this system? That people with setbacks or irregularities in their work life were harmed.

Therefore, this new system allows you to choose between the current form or the new formula that takes into account the last 29 years of contributions, that is, 348 months, but allowing the 24 monthly payments with the lowest contributions to be excluded. Now, it will not be all at once, it will start from January 1, 2026 and will take the best 304 months, being able to download the two worst months (table with the new dual system).

Table with the percentage of the pension based on the years of contributions

The regulatory base will be taken following this new method, but taking into account that the percentage of said base will depend on the total number of years of contributions, that is, the more years the higher the percentage until reaching 100%. Thus, to access the contributory retirement pension it will be necessary to have a minimum of 15 years of contributions, which will give the right to 50% of the regulatory base. From this minimum, the following percentages apply:

- For each additional month of the next 49 months, an extra 0.21% of the regulatory base will be added.

- For each additional month up to month 209, an extra 0.19% of the regulatory base will be added.

In this way, workers who have been contributing for at least 36 years and 6 months will be entitled to 100% of the pension. This will be valid for 2026, but as stated in Law 27/2011, in 2027 it will change and a total of 37 years of contributions will be necessary.

This would be the table based on the years quoted for 2026

| Listed Years | Regulatory Base Percentage |

|---|---|

| 15 | 50% |

| 16 | 52.52% |

| 17 | 55.04% |

| 18 | 57.56% |

| 19 | 60.08% |

| 20 | 62.50% |

| 21 | 64.82% |

| 22 | 67.14% |

| 23 | 69.46% |

| 24 | 71.78% |

| 25 | 74.10% |

| 26 | 76.38% |

| 27 | 78.66% |

| 28 | 80.94% |

| 29 | 83.22% |

| 30 | 85.50% |

| 31 | 87.78% |

| 32 | 90.06% |

| 33 | 92.34% |

| 34 | 94.62% |

| 35 | 96.90% |

| 36 years and six months or more | 100% |

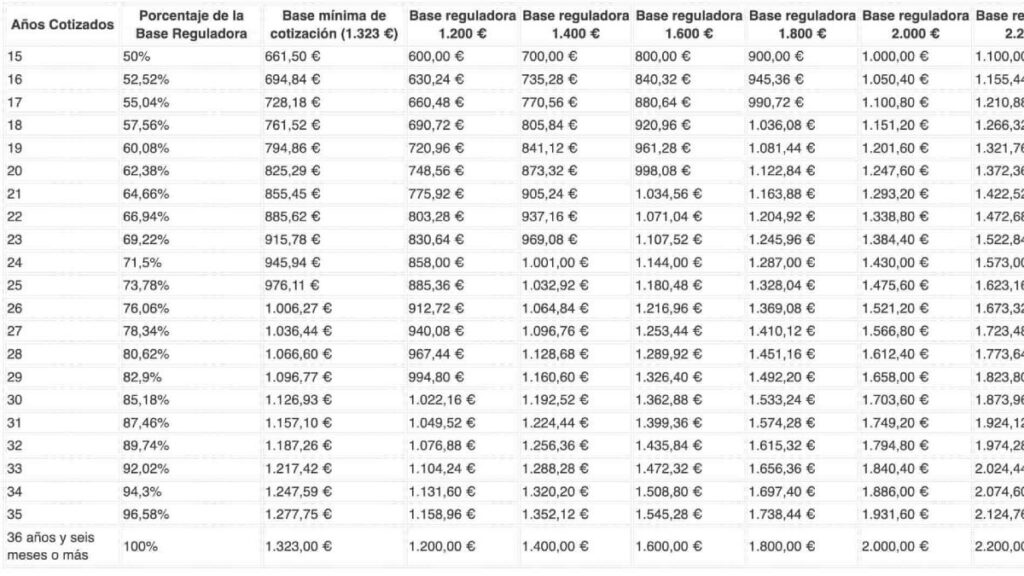

This is how the retirement pension would look depending on the regulatory basis:

What pension do I have depending on the years of contributions according to my salary?

In the case of knowing the total number of years of contributions and the regulatory basis, the following table can be used as a guideline to see what our future retirement pension will be.

| Listed Years | Regulatory Base Percentage | Minimum contribution base (€1,323) | Regulatory base €1,200 | Regulatory base €1,400 | Regulatory base €1,600 | Regulatory base €1,800 | Regulatory base €2,000 | Regulatory base €2,200 |

|---|---|---|---|---|---|---|---|---|

| 15 | 50% | €661.50 | €600.00 | €700.00 | €800.00 | €900.00 | €1,000.00 | €1,100.00 |

| 16 | 52.52% | €694.84 | €630.24 | €735.28 | €840.32 | €945.36 | €1,050.40 | €1,155.44 |

| 17 | 55.04% | €728.18 | €660.48 | €770.56 | €880.64 | €990.72 | €1,100.80 | €1,210.88 |

| 18 | 57.56% | €761.52 | €690.72 | €805.84 | €920.96 | €1,036.08 | €1,151.20 | €1,266.32 |

| 19 | 60.08% | €794.86 | €720.96 | €841.12 | €961.28 | €1,081.44 | €1,201.60 | €1,321.76 |

| 20 | 62.38% | €825.29 | €748.56 | €873.32 | €998.08 | €1,122.84 | €1,247.60 | €1,372.36 |

| 21 | 64.66% | €855.45 | €775.92 | €905.24 | €1,034.56 | €1,163.88 | €1,293.20 | €1,422.52 |

| 22 | 66.94% | €885.62 | €803.28 | €937.16 | €1,071.04 | €1,204.92 | €1,338.80 | €1,472.68 |

| 23 | 69.22% | €915.78 | €830.64 | €969.08 | €1,107.52 | €1,245.96 | €1,384.40 | €1,522.84 |

| 24 | 71.5% | €945.94 | €858.00 | €1,001.00 | €1,144.00 | €1,287.00 | €1,430.00 | €1,573.00 |

| 25 | 73.78% | €976.11 | €885.36 | €1,032.92 | €1,180.48 | €1,328.04 | €1,475.60 | €1,623.16 |

| 26 | 76.06% | €1,006.27 | €912.72 | €1,064.84 | €1,216.96 | €1,369.08 | €1,521.20 | €1,673.32 |

| 27 | 78.34% | €1,036.44 | €940.08 | €1,096.76 | €1,253.44 | €1,410.12 | €1,566.80 | €1,723.48 |

| 28 | 80.62% | €1,066.60 | €967.44 | €1,128.68 | €1,289.92 | €1,451.16 | €1,612.40 | €1,773.64 |

| 29 | 82.9% | €1,096.77 | €994.80 | €1,160.60 | €1,326.40 | €1,492.20 | €1,658.00 | €1,823.80 |

| 30 | 85.18% | €1,126.93 | €1,022.16 | €1,192.52 | €1,362.88 | €1,533.24 | €1,703.60 | €1,873.96 |

| 31 | 87.46% | €1,157.10 | €1,049.52 | €1,224.44 | €1,399.36 | €1,574.28 | €1,749.20 | €1,924.12 |

| 32 | 89.74% | €1,187.26 | €1,076.88 | €1,256.36 | €1,435.84 | €1,615.32 | €1,794.80 | €1,974.28 |

| 33 | 92.02% | €1,217.42 | €1,104.24 | €1,288.28 | €1,472.32 | €1,656.36 | €1,840.40 | €2,024.44 |

| 34 | 94.3% | €1,247.59 | €1,131.60 | €1,320.20 | €1,508.80 | €1,697.40 | €1,886.00 | €2,074.60 |

| 35 | 96.58% | €1,277.75 | €1,158.96 | €1,352.12 | €1,545.28 | €1,738.44 | €1,931.60 | €2,124.76 |

| 36 years and six months or more | 100% | €1,323.00 | €1,200.00 | €1,400.00 | €1,600.00 | €1,800.00 | €2,000.00 | €2,200.00 |