Social security allows certain workers with long contribution careers to advance their retirement age through the known as early retirement. In the case of the voluntary modality, it is possible to anticipate up to two years regarding the ordinary retirement age. However, this option entails a reduction in the amount of the pension, which will be greater or lesser depending on the total of quoted years and the months that retirement is forward.

In 2025, the ordinary retirement legal age is set at 66 years and 8 months, except for those who accredit at least 38 years and three months quoted, in which case they can retire at 65. This means that voluntary anticipated retirement can be accessed from 63 years if the 38 years and three months of contribution are exceeded, or from 64 years and 8 months if at least 35 years have been quoted, which is the minimum price requirement required for this modality.

You may be interested

Tara (59 years): “I wanted to ask for early retirement in the United States, but it was impossible to live near the beach even with all my savings and moved to Spain”

Retirees explode against Social Security: “They say it costs a lot

In addition, Social Security asks that the resulting pension (the one received by the pensioner) is superior to the amount of the minimum pension that would correspond to the beneficiary based on their family situation when they turn 65.

Now, many wonder why penalty if only those with long contribution races can access, that is, the workers who contributed the most to the system. The answer is that Social Security understands that, by enjoying before the pension and, therefore, for a longer period of it, it has to be cut so as not to stress the public pension system. In addition, the latest reforms applied by the Government of Pedro Sánchez sought precisely that: discouraging early retirements and rewarding the delay, to get as much as possible to the real retirement age.

Up to a room less than the pension

Voluntary early retirement entails the application of reducing coefficients that can reduce the pension between 2.81% and 21%, depending on the number of quoted years and the months of the removal. This “penalty” is applied once the pension regulatory base is calculated, and is regulated by the new monthly coefficient system introduced by the pension reform of 2022, in force in 2025.

These are some approximate examples of reduction for those who advance their retirement two years (24 months) or a single month, according to the quoted years:

- Less than 38 years and 6 months quoted: up to 21% reduction if they retire two years earlier, and around 3.26% if only one month is advanced.

- Between 38 years and 6 months and 41 years and 6 months quoted: around 19% cut with two years of advance, and about 3.11% if it is a month earlier.

- Between 41 years and 6 months and 44 years and 6 months quoted: 17% reduction with two years of advance, and 2.86% if it is a month earlier.

- More than 44 years and 6 months quoted: the penalty drops to 13% if two years are carried out, and to 2.81% if it is anticipated only one month.

| Months that retirement advances | Less than 38 years and 6 months quoted | More than 38 years and 6 months quoted and less than 41 years and 6 months | More than 41 years and 6 months quoted and less than 44 years and 6 months | 44 years and 6 months or more contribution |

|---|---|---|---|---|

| 24 | 21% | 19% | 17% | 13% |

| 23 | 17.60% | 16.50% | 15% | 12% |

| 22 | 14.67% | 14% | 13.33% | 11% |

| 21 | 12.57% | 12% | 11.43% | 10% |

| 20 | 11% | 10.50% | 10% | 9.20% |

| 19 | 9.78% | 9.33% | 8.89% | 8.40% |

| 18 | 8.80% | 8.40% | 8% | 7.60% |

| 17 | 8% | 7.64% | 7.27% | 6.91% |

| 16 | 7.33% | 7% | 6.67% | 6.33% |

| 15 | 6.77% | 6.46% | 6.15% | 5.85% |

| 14 | 6.29% | 6% | 5.71% | 5.43% |

| 13 | 5.87% | 5.60% | 5.33% | 5.07% |

| 12 | 5.50% | 5.25% | 5% | 4.75% |

| 11 | 5.18% | 4.94% | 4.71% | 4.47% |

| 10 | 4.89% | 4.67% | 4.44% | 4.22% |

| 9 | 4.63% | 4.42% | 4.21% | 4% |

| 8 | 4.40% | 4.20% | 4% | 3.80% |

| 7 | 4.19% | 4% | 3.81% | 3.62% |

| 6 | 4% | 3.82% | 3.64% | 3.45% |

| 5 | 3.83% | 3.65% | 3.48% | 3.30% |

| 4 | 3.67% | 3.50% | 3.33% | 3.17% |

| 3 | 3.52% | 3.36% | 3.20% | 3.04% |

| 2 | 3.38% | 3.23% | 3.08% | 2.92% |

| 1 | 3.26% | 3.11% | 2.96% | 2.81% |

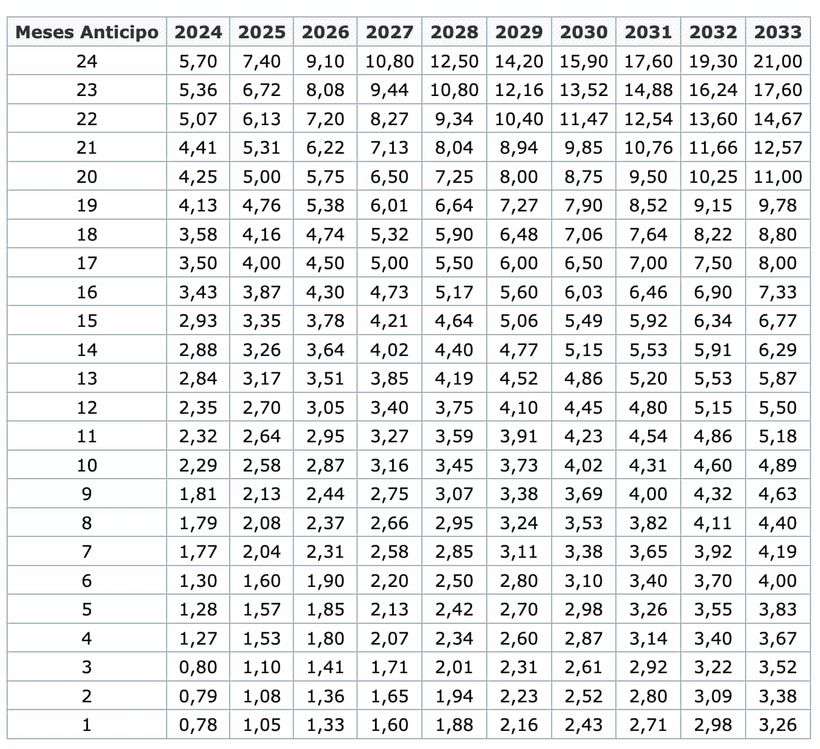

If the pension exceeds the maximum amount an extra cut will be applied

Now, it must be borne in mind that if after applying the calculation method, the resulting pension was greater than the maximum pension, social security will apply a new reducing trust, that is, the maximum pension can never be charged. This coefficient varies as in early retirement, of the total quoted years and the months advanced. These coefficients are published under the Trigeasima Fourth transitory provision of Law 21/2021 (published in this Official State Gazette), being the following table for this year 2025.

| Months of advance | Less than 38 years and 6 months | Equal to or greater than 38 years and 6 months and less than 41 years and 6 months | Equal to or greater than 41 years and 6 months and less than 44 years and 6 months | Over 44 years and 6 months |

|---|---|---|---|---|

| 24 | 7.40% | 7.00% | 6.60% | 5.80% |

| 23 | 6.72% | 6.50% | 6.20% | 5.60% |

| 22 | 6.13% | 6.00% | 5.87% | 5.40% |

| 21 | 5.31% | 5.20% | 5.09% | 4.80% |

| 20 | 5.00% | 4.90% | 4.80% | 4.64% |

| 19 | 4.76% | 4.67% | 4.58% | 4.48% |

| 18 | 4.16% | 4.08% | 4.00% | 3.92% |

| 17 | 4.00% | 3.93% | 3.85% | 3.78% |

| 16 | 3.87% | 3.80% | 3.73% | 3.67% |

| 15 | 3.35% | 3.29% | 3.23% | 3.17% |

| 14 | 3.26% | 3.20% | 3.14% | 3.09% |

| 13 | 3.17% | 3.12% | 3.07% | 3.01% |

| 12 | 2.70% | 2.65% | 2.60% | 2.55% |

| 11 | 2.64% | 2.59% | 2.54% | 2.49% |

| 10 | 2.58% | 2.53% | 2.49% | 2.44% |

| 9 | 2.13% | 2.08% | 2.04% | 2.00% |

| 8 | 2.08% | 2.04% | 2.00% | 1.96% |

| 7 | 2.04% | 2.00% | 1.96% | 1.92% |

| 6 | 1.60% | 1.56% | 1.53% | 1.49% |

| 5 | 1.57% | 1.53% | 1.50% | 1.46% |

| 4 | 1.53% | 1.50% | 1.47% | 1.43% |

| 3 | 1.10% | 1.07% | 1.04% | 1.01% |

| 2 | 1.08% | 1.05% | 1.02% | 0.98% |

| 1 | 1.05% | 1.02% | 0.99% | 0.96% |

As the law explains, these “penalties are by 2025” and they will increase every year, until 2033 when social security may take up to 21% in the case of being less than 38 years and six months quoted.

Is it possible to retire without penalty?

No, at least through the voluntary anticipated retirement modality. Now, the Social Security System allows to adapt to the work need of each worker. Thus, for example, workers whose professions where working conditions are exceptionally difficult, dangerous, toxic or unhealthy, and where high rates of disease or mortality are observed may benefit from a reduction in retirement age.

Another way is through the anticipated retirement for disability in which workers do not suffer cuts over their quotation years. Depending on the degree of disability they can advance it up to a maximum of 52 or 56 years.