For Social Security, the amount of the early retirement pension depends on three factors: regulatory base, the total years of contributions and the months in which retirement is brought forward about the ordinary age. While the first determines 100% of the retirement pension to which one is entitled, the second will act to know what part of that 100% corresponds. Finally, depending on the months in advance, Social Security will apply a reducing coefficient that can range from 0.50% to 30%.

As we have said, the regulatory base is the 100% of the pension to which you are entitled based on the years of contributions and that should not be confused with the maximum pension. To be entitled to 100% it is necessary to contribute at least 36 years and six months, but as long as you reach the ordinary age. This is calculated by dividing the last 300 contribution bases by 350.

In this calculation two aspects must be taken into account. On the one hand, the possibility of integrating contribution gaps, which allow filling in the periods in which contributions could not be made with “fictitious contributions” (article 209 of the General Social Security Law). On the other hand, and to avoid the loss of purchasing power, all contribution bases, except those of the last two years, will be updated by applying a coefficient to reflect the inflation effect. The bases for the last two years are calculated at their nominal value, that is, without adjusting for inflation.

Now, Social Security advance the legal age to enjoy the pension before through early retirement. This can be volunteerwhich allows you to advance up to two years with respect to the ordinary age, or involuntary (beyond the control of a worker, such as an ERE) that allows access to the public pension up to four years in advance. In both modalities it will be necessary to meet a series of requirements, in addition to knowing that reducing coefficients will be applied, as we have already mentioned.

Early retirement is the possibility of any worker receiving a public retirement pension before the legal retirement age. This can be voluntary, which allows you to advance up to two years with respect to the ordinary age, or involuntary (beyond the will of a worker such as an ERE), which allows access to the public pension up to four years in advance. In both modalities, a series of requirements will need to be met.

Table with the pension percentage based on the years of contributions

Depending on the years of contributions, you are entitled to a percentage of the regulatory base. With 15 years of contributions, which is the minimum to access a contributory pension, you are entitled to 50% of the regulatory base. From there, the following coefficients will be applied:

- For each month contributed during the next 49 months, an extra 0.21% of the regulatory base is added.

- After those 49 months, for each of the additional 209 months, 0.19% is added.

Thus, to be entitled to 100% it is necessary to have been contributing for 36 years and six months, this calculation being valid for 2025 and 2026. As of 2027 it will change, applying the new dual calculation method and with other coefficients. This is how the percentage would look depending on the years worked:

| Listed Years | Regulatory Base Percentage |

|---|---|

| 15 | 50% |

| 16 | 52.52% |

| 17 | 55.04% |

| 18 | 57.56% |

| 19 | 60.08% |

| 20 | 62.38% |

| 21 | 64.66% |

| 22 | 66.94% |

| 23 | 69.22% |

| 24 | 71.50% |

| 25 | 73.78% |

| 26 | 76.06% |

| 27 | 78.34% |

| 28 | 80.62% |

| 29 | 82.90% |

| 30 | 85.18% |

| 31 | 87.46% |

| 32 | 89.74% |

| 33 | 92.02% |

| 34 | 94.30% |

| 35 | 96.58% |

| 36 years and six months or more | 100% |

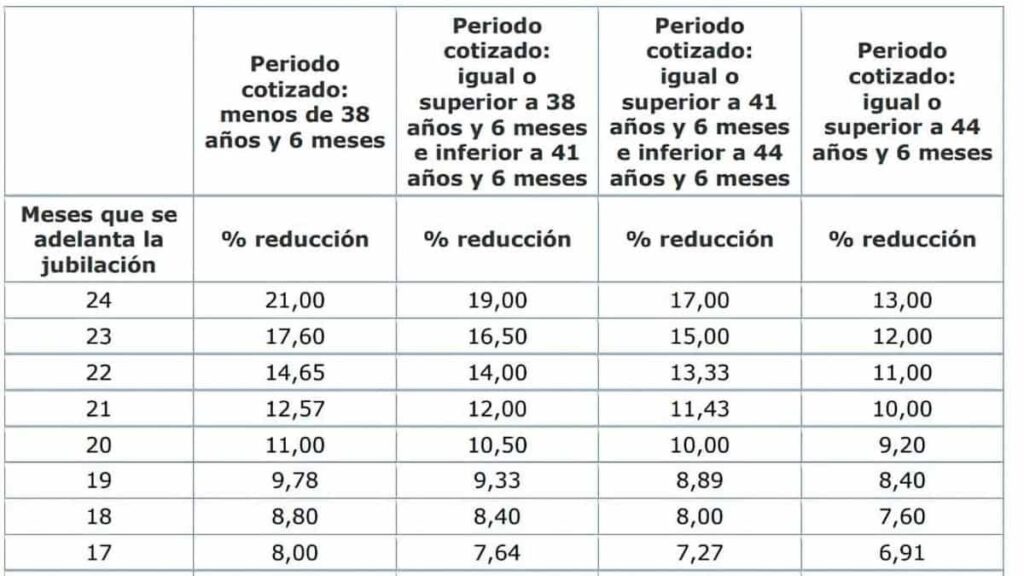

Table with penalties for voluntary early retirement

In voluntary retirements, Social Security applies reducing coefficients based on the years of contributions and the months in advance. This ranges between 2.81% and 21%, depending on the years of contributions and the time in advance of retirement. These would be the penalties:

- Less than 38 years and six months of contributions: 21% reduction if 2 years early; 3.26% if it is a month before.

- Between 38 years and six months and 41 years and six months: 19% cut if 2 years early; 3.11% if it is a month before.

- Between 41 years and six months and 44 years and six months: 17% cut if 2 years early; 2.86% if it is a month before.

- More than 44 years and six months of contributions: 13% reduction if 2 years early; 2.81% if it is a month before.

In the following table you can see what it would look like according to the months ahead and the years quoted:

| Retirement months early | Less than 38 years and 6 months | Less than 41 years and 6 months | Less than 44 years and 6 months | 44 years and 6 months or more |

|---|---|---|---|---|

| 24 | 21% | 19% | 17% | 13% |

| 23 | 17.60% | 16.50% | 15% | 12% |

| 22 | 14.65% | 14% | 13.33% | 11% |

| 21 | 12.57% | 12% | 11.43% | 10% |

| 20 | 11% | 10.50% | 10% | 9.20% |

| 19 | 9.78% | 9.33% | 8.89% | 8.40% |

| 18 | 8.80% | 8.40% | 8% | 7.60% |

| 17 | 8% | 7.64% | 7.27% | 6.91% |

| 16 | 7.33% | 7% | 6.67% | 6.33% |

| 15 | 6.77% | 6.46% | 6.15% | 5.85% |

| 14 | 6.29% | 6% | 5.71% | 5.43% |

| 13 | 5.87% | 5.60% | 5.33% | 5.07% |

| 12 | 5.50% | 5.25% | 5% | 4.75% |

| 11 | 5.18% | 4.94% | 4.71% | 4.47% |

| 10 | 4.89% | 4.67% | 4.44% | 4.22% |

| 9 | 4.63% | 4.42% | 4.21% | 4% |

| 8 | 4.40% | 4.20% | 4% | 3.80% |

| 7 | 4.19% | 4% | 3.81% | 3.62% |

| 6 | 4% | 3.82% | 3.64% | 3.45% |

| 5 | 3.83% | 3.65% | 3.48% | 3.30% |

| 4 | 3.67% | 3.50% | 3.33% | 3.17% |

| 3 | 3.52% | 3.36% | 3.20% | 3.04% |

| 2 | 3.38% | 3.23% | 3.08% | 2.92% |

| 1 | 3.26% | 3.11% | 2.96% | 2.81% |

In this way, for example, a worker with a regulatory base of 2,200 euros who had worked 36 years and brought forward his retirement by 12 months would see a penalty of 5.50% applied according to the table of reducing coefficients. This would mean a reduction of 121 euros per month, leaving an approximate pension of 2,079 euros per month. This calculation is applied to each of the 14 annual payments.

Table of penalties for involuntary early retirement

In forced early retirements, Penalties will range from 0.50% (when withdrawal is advanced one month) up to 30% (for a maximum of 48 months with less than 38 years of contributions). The reducing coefficients are applied progressively according to the years contributed:

- With less than 38 years and six months of contributions: 30% reduction if the advance is for four years, 22.50% if it is for three, 15% if it is for two, and 5.50% if it is for one year.

- Between 38 years and six months and 41 years and six months of contributions: 28% cut if the advance is for four years, 21% if it is for three, 14% if it is for two, and 5.25% if it is for one year .

- Between 41 years and six months and 44 years and six months of contributions: 26% reduction if the advance is for four years, 19.50% if it is for three, 13% if it is for two, and 5% if it is for one year .

- With more than 44 years and six months of contributions: 24% reduction if the retirement occurs four years in advance, 18% if it is three, 12% if it is two, and 4.75% if it is one year.

| Retirement months early | Less than 38 years and 6 months | Less than 41 years and 6 months | Less than 44 years and 6 months | 44 years and 6 months or more |

|---|---|---|---|---|

| 4 years – 48 | 30% | 28% | 26% | 24% |

| 47 | 29.4% | 27.4% | 25.5% | 23.5% |

| 46 | 28.8% | 26.8% | 24.9% | 23 % |

| 45 | 28.1% | 26.3% | 24.4% | 22.5% |

| 44 | 27.5% | 25.7% | 23.8% | 22% |

| 43 | 26.9% | 25.1% | 23.3% | 21.5% |

| 42 | 26.25% | 24.5% | 22.8% | 21% |

| 41 | 25.6% | 23.9% | 22.2% | 20.5% |

| 40 | 25% | 23.3% | 21.7% | 20% |

| 39 | 24.4% | 22.8% | 21.1% | 19.5% |

| 38 | 23.8% | 22.2% | 20.6% | 19% |

| 37 | 23.1% | 21.6% | 20% | 18.5% |

| 3 years – 36 | 22.5% | 21% | 19.5% | 18% |

| 35 | 21.9% | 20.4% | 19% | 17.5% |

| 34 | 21.3% | 19.8% | 18.4% | 17% |

| 33 | 20.6% | 19.3% | 17.9% | 16.5% |

| 32 | 20% | 18.7% | 17.3% | 16% |

| 31 | 19.4% | 18.1% | 16.8% | 15.5% |

| 30 | 18.8% | 17.5% | 16.3% | 15% |

| 29 | 18.1% | 16.9% | 15.7% | 14.5% |

| 28 | 17.5% | 16.3% | 15.2% | 14% |

| 27 | 16.9% | 15.8% | 14.6% | 13.5% |

| 26 | 16.3% | 15.2% | 14.1% | 13% |

| 25 | 15.6% | 14.6% | 13.5% | 12.5% |

| 2 years – 24 | 15% | 14% | 13% | 12% |

| 23 | 14.4% | 13.4% | 12.5% | 11.5% |

| 22 | 13.8% | 12.8% | 11.9% | 11% |

| 21 | 12.6% | 12% | 11.4% | 10% |

| 20 | 11% | 10.5% | 10% | 9.2% |

| 19 | 9.78% | 9.33% | 8.89% | 8.4% |

| 18 | 8.8% | 8.4% | 8% | 7.6% |

| 17 | 8% | 7.64% | 7.27% | 6.91% |

| 16 | 7.33% | 7% | 6.67% | 6.33% |

| 15 | 6.77% | 6.46% | 6.15% | 5.85% |

| 14 | 6.29% | 6% | 5.71% | 5.43% |

| 13 | 5.87% | 5.6% | 5.33% | 5.07% |

| 1 year – 12 | 5.5% | 5.25% | 5% | 4.75% |

| 11 | 5.18% | 4.94 | 4.71% | 4.47% |

| 10 | 4.89% | 4.67% | 4.44% | 4.22% |

| 9 | 4.63% | 4.42% | 4.21% | 4% |

| 8 | 4.4% | 4.2% | 4% | 3.8% |

| 7 | 4.19% | 4% | 3.81% | 3.62% |

| 6 | 3.75% | 3.5% | 3.25% | 3% |

| 5 | 3.13% | 2.92% | 2.71% | 2.5% |

| 4 | 2.5% | 2.33% | 2.17% | 2% |

| 3 | 1.88% | 1.75% | 1.63% | 1.5% |

| 2 | 1.25% | 1.17% | 1.08% | 1% % |

| 1 | 0.63% | O.58% | O.54% | Or,50% |

| 0 | – | – | – | – |

For example, a worker with a regulatory base of 2,200 euros who has contributed for 38 years and advances his retirement involuntarily by 24 months, would suffer a penalty of 28% according to the corresponding table. This translates into a reduction of 616 euros per month, leaving your pension at approximately 1,584 euros per month. This amount is applied to each of the 14 annual payments.

Penalty for early retirement when the maximum pension is exceeded

In the event that, after applying the reducing coefficients, the resulting pension is higher than the maximum pension, Social Security will apply a reducing coefficient so that it does not reach said quantity. The application of these reducing coefficients will be done in such a way that the recognized pension is not lower than what would have corresponded applying the rules in force in 2021.

The application of these reducing coefficients will be done in such a way that the pension recognized is not lower than what would have corresponded applying the rules in force in 2021.

| Months Advance | Less than 38 years and six months | more than 38 years and 6 months and less than 41 years and 6 months | More than 41 years and 6 months and less than 44 years and 6 months | Equal to or greater than 44 years and 6 months |

|---|---|---|---|---|

| 24 months | 7.4% | 7.0% | 6.6% | 5.8v |

| 23 months | 6.72% | 6.5% | 6.2% | 5.6% |

| 22 months | 6.13% | 6.0% | 5.87% | 5.4% |

| 21 months | 5.31% | 5.2% | 5.09% | 4.8% |

| 20 months | 5.0% | 4.9% | 4.8% | 4.64% |

| 19 months | 4.76% | 4.67% | 4.58% | 4.48% |

| 18 months | 4.16% | 4.08% | 4.0% | 3.92% |

| 17 months | 4.0% | 3.93% | 3.85% | 3.78% |

| 16 months | 3.87% | 3.8% | 3.73% | 3.67% |

| 15 months | 3.35% | 3.29% | 3.23% | 3.17% |

| 14 months | 3.26% | 3.2% | 3.14% | 3.09% |

| 13 months | 3.17% | 3.12% | 3.07% | 3.01% |

| 12 months | 2.7% | 2.65% | 2.6% | 2.55% |

| 11 months | 2.64 | 2.59 | 2.54 | 2.49 |

| 10 months | 2.58 | 2.53 | 2.49 | 2.44 |

| 9 months | 2.13 | 2.08 | 2.04 | 2.0 |

| 8 months | 2.04 | 2.04 | 2.0 | 1.96 |

| 7 months | 2.04 | 2.0 | 1.96 | 1.92 |

| 6 months | 1.6 | 1.56 | 1.53 | 1.49 |

| 5 months | 1.57 | 1.53 | 1.5 | 1.46 |

| 4 months | 1.53 | 1.5 | 1.47 | 1.43 |

| 3 months | 1.1 | 1.07 | 1.04 | 1.01 |

| 2 months | 1.08 | 1.05 | 1.02 | 0.98 |

| 1 months | 1.05 | 1.02 | 0.99 | 0.96 |