The payroll is the document detailing both the agreed salary and the deductions applied to the Treasury and Social Security. In addition, it serves as a proof that the worker has received his salary and that the payments corresponding to Social Security and the withholdings of the IRPF have been made. To ensure that the payment is correct, it is essential to review two key aspects that are the contribution group and seniority.

To verify it, it must be borne in mind that, although most payrolls have different designs, all must comply with a model established as provided in the ESS/2098/2014 order (consultable in this Official State Gazette) and in compliance with article 104.2 of the General Social Security Law. This means that payroll must follow a specific format that mandatory a series of concepts.

You may be interested

Check your payroll: If your company has not paid you on the corresponding date you could claim 10% more salary

Pablo Casas, a young Spanish who lives in Switzerland: “Working 11 hours as washing, cutting your hands or enduring insults in French that you don’t even understand, it is not a good taste dish for anyone”

In this way, all workers can understand how a payroll works regardless of the company in which they work, since the concepts will always be the same. Now, these are the two concepts to be reviewed on a payroll.

Contribution group

The contribution group, indicated as “GC” or “rate” on the payroll, indicates the professional category of the worker, defined according to the corresponding collective agreement. This data is fundamental, since each category is assigned a minimum wage and contribution bases that impact both the monthly salary and in future rights, such as the retirement pension. The contribution groups, ordered from highest to lowest, are the following:

- Engineers and graduates

- Technical engineers and assistants entitled

- Administrative and Workshop Chiefs

- Non -titled Assistants

- Administrative Officers

- Subaltern

- Administrative assistants

- First, Second and Third Officers

- Pawns

- Workers under 18, regardless of their category

Ensure that the contribution group is correct guarantees that salary and contributions are adjusted to the minimum established for the position, avoiding salary losses or inappropriate quotes. For example, if a worker develops a professional activity above his contribution group, although this is not reflected in his salary, he could negatively affect the future, as in the amount of his retirement pension, since he would be quoting for a base lower than expected.

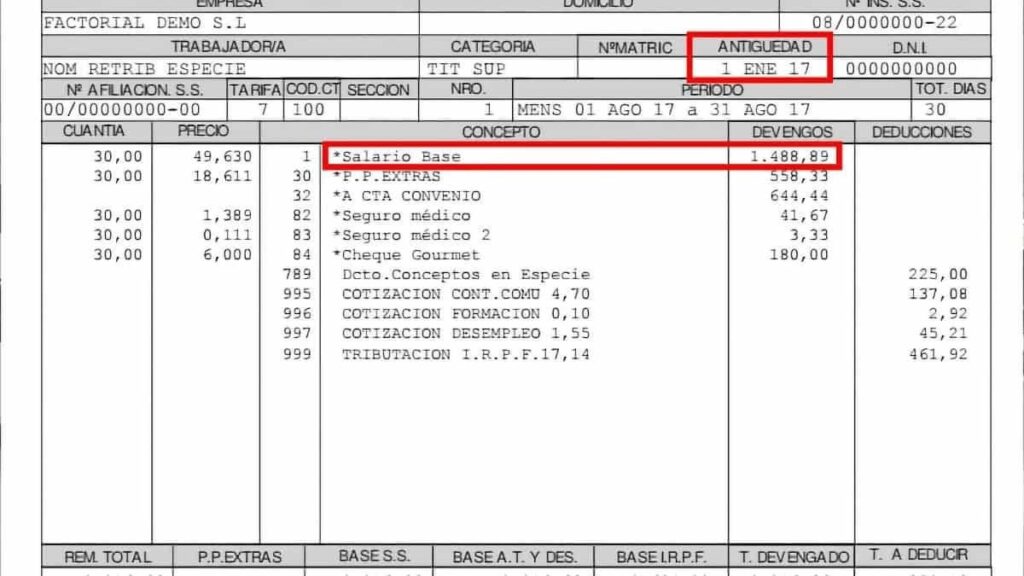

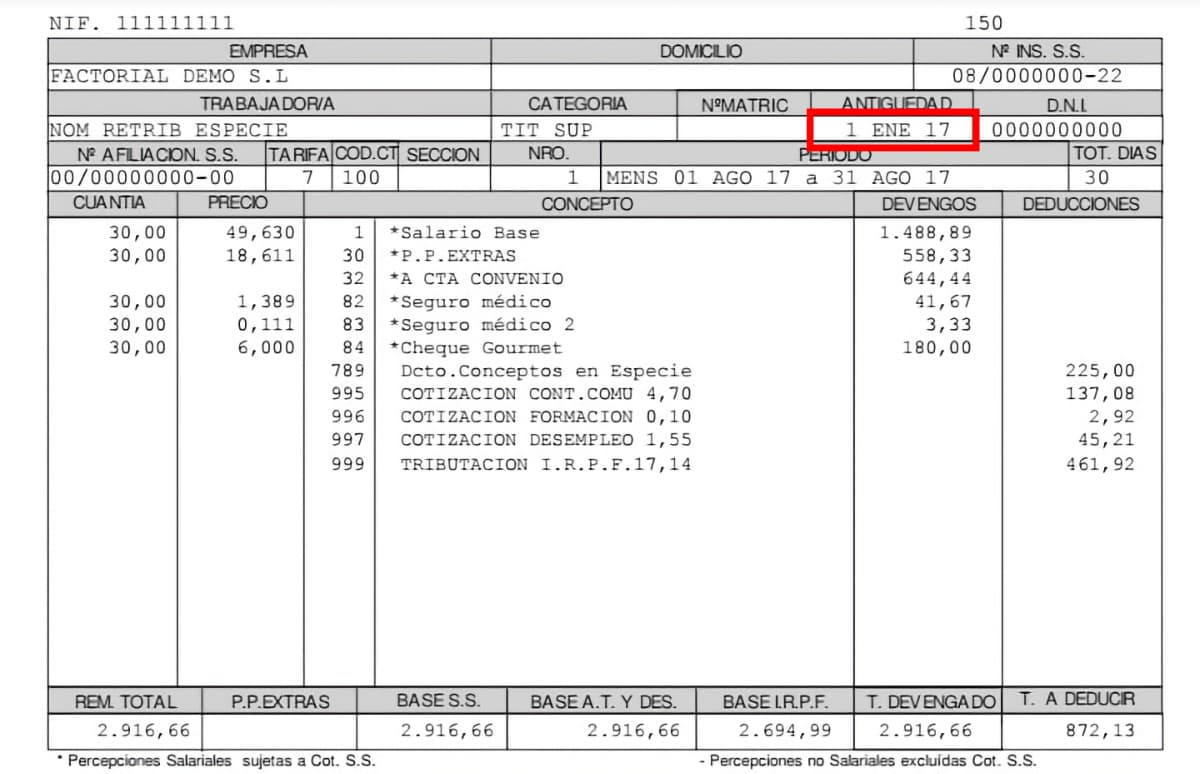

Antiquity in the company

Antiquity influences the calculation of a possible compensation for dismissal and the increase in the base salary, stipulated in the collective agreement. In general, the greater the base salary, something that directly impacts the payroll.

Difference between gross and net salary

In addition to these two important concepts in the payroll and that we must often review, it is important to understand other concepts, such as the difference between gross salary and net salary. The gross salary will always be greater than the net, since it represents the total amount that an employee earns and that appears on his payroll before applying the corresponding withholdings and contributions. That is, the gross salary is the sum of the base salary plus accessories. In collective agreements and salary tables, the salary of each worker is specified in terms of gross salary, not of net salary.

On the other hand, the net salary is the exact amount that the worker receives as consideration for his services, after discounting the social security contributions and the retaining of the personal income tax (income tax of the natural persons). In other words, it is the real money available for the worker after fulfilling his fiscal and contribution obligations.

How to understand a payroll

For any worker it is necessary to know how to read and understand his payroll to verify that what the company is paying is correct. In the following list each concept can be summarized:

- Base salary: represents the minimum remuneration the worker receives for his services. This amount cannot be lower than that established by the collective agreement for the worker’s group or professional category, which must appear indicated in the payroll.

- Antiquity: This complement increases the salary as the years go by in the company. It is calculated as a percentage of the base salary and is applied after a certain period, as specified in the collective agreement. The payroll does not always include the start date of the contract, so it must be reviewed.

- Salary concepts: the payroll can include several additional salary concepts, such as accessories for productivity, responsibility, nocturnity, among others. These concepts may vary according to the company’s policy. In some cases, although in theory the salary has been increased, the net amount received may not change due to modifications in these concepts.

- Payments in kind: Some employees receive part of their salary in the form of non -monetary benefits, such as food or transport checks. These payments in kind cannot exceed 30% of the total remuneration and, although they are additional benefits, the cash salary receiving the worker can never be lower than the current interprofessional minimum salary (SMI).

- Deductions: These are the amounts that are subtracted from the gross salary to cover the social security contributions and IRPF (Income Tax of natural persons). These deductions finance rights such as pension, unemployment insurance and casualties due to disability.

- Retention percentage: IRPF is calculated based on the salary and the family situation of the worker. It is important to communicate any personal change, such as marriage or birth of children, to adjust retention correctly.

- Annual gross salary: it is the total income before deductions in a year and is calculated from the price indicated on the payroll. This data allows us to verify that the agreed annual salary complies with the provisions of the contract or agreement.