The approval in the Congress of Deputies of the motion presented by Podemos to eliminate the reducing coefficients in the early retirements of those who have contributed for more than 40 years has once again put on the table a right that 900,000 retirees in Spain have been demanding. These pensioners still wonder why they should be “penalized for life” after being the ones who contributed the most to Social Security.

The initiative went ahead with a large majority, with 180 votes in favor and 170 abstentions, which were those of the Popular Party and Vox. Although the motion is not legislative in nature, it does urge the Government to modify the regulations to correct this situation. And behind this parliamentary victory there is a proper name, being Asjubi40an association that represents more than 900,000 pensioners and that has been defending for years that these penalties violate the principle of contributory system.

You may be interested

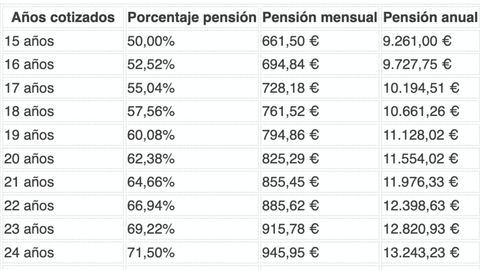

Table with the retirement pension that you will have according to the years of contributions if you receive the Minimum Interprofessional Wage

Social Security denies raising the retirement age to 70 years and guarantees the future of pensions

Alfonso Muñoz Cuenca, a Social Security official specialized in pensions, has published a video where he talks about this topic and explains, point by point, why he considers it essential to eliminate these penalties.

“Applying reducing coefficients to those who have contributed for more than 40 years violates taxability”

To understand the scope of the debate, Muñoz recalls the five pillars of the public pension system: distribution, contributory proportionality, universality, public management and economic sufficiency. And it is precisely on the principle of proportionality where he places the focus, where he explains that “if a worker has contributed for more than 40 years, how is it possible that, for retiring a few months early, a lifetime penalty is applied that places him at the same percentage as someone who has only contributed for 26 years? Penalizing like this violates the internal logic of the system.”

In this sense, Alfonso insists that greater contribution, that is, more years worked, should always correspond to a better pension. That is why he considers that maintaining these cuts is an anomaly within the model itself.

In his analysis, Muñoz explains a case that, in his opinion, shows the breach of the principle of contributory. “A worker who reaches his ordinary age with only 26 years of contributions receives 76% of his pension. However, another worker who has contributed 45 years and decides to retire four years earlier also receives 76%. The system is equalizing those who have contributed half,” says the official.

From there, he introduces a comparison that, according to him, is equally difficult to justify. “An official included in the Passive Classes regime can retire with 100% of his pension at age 65 as long as he has 35 years of contributions,” he explains. On the other hand, in the General Regime “it is required to reach the age of 67 and prove 36 and a half years of contributions (37 in 2027) to be able to collect the full pension.”

But it doesn’t stop there, since the differences widen when that career path is not reached. Muñoz recalls that “in Passive Classes a linear reduction coefficient of 3.65% is applied for each missing year”, while in the General Regime “the penalty ranges between 4.75% and 10.5% for each year of anticipation”, although this depends on the total number of years of contributions and whether early retirement is voluntary or involuntary.

To understand it better, the official gives the following practical example. “A public employee with 35 years of contributions would suffer a penalty of 7.3%, while a General Regime worker with 40 years of contributions who retires only two years earlier would endure a 19% cut. And all of this having contributed seven more years.” Thus, for Muñoz, this is one of the clearest examples of the structural inequality generated by the current system of penalties.

These retirees lose up to 200,000 euros

Muñoz recalls that these workers who have to retire early (often forced) lose a lot of money in their pension. Thus, according to the calculations of Asjubi40, “a Passive Class official with 35 years of contributions can receive around 800,000 euros as a pensioner, while a General Regime worker who retires at his ordinary age receives around 600,000 euros and another with 45 years of contributions who anticipate their retirement four years barely reach 582,000For the official, these differences do not respond to contributory criteria, but rather to structural cuts that do not take into account the real effort of long working careers.

The Government, however, maintains that correcting this situation would have a high cost. Muñoz recalls that the Ministry of Social Security estimated the impact of eliminating the reducing coefficients at 2.7 billion euros annually. In a 2021 report, José Luis Escrivá defended its maintenance by pointing out that “anticipating retirement has a cost for the system”, that only 23% of these retirements affect women and that compensation mechanisms already exist for very long careers. Muñoz questions this reasoning with a forceful phrase: “Since when are injustices corrected or not depending on their economic cost?”

The official insists that many workers with more than 40 years of contributions do not anticipate their retirement of their own volition, but rather due to layoffs at age 60 or 61, health problems or the impossibility of returning to the labor market. To this he adds that there are groups such as firefighters and local police who can retire without penalty, while others with 40, 45 and even 50 years of contributions endure cuts for life.

Furthermore, he emphasizes that “pensioners are local consumers”, so the elimination of these penalties would also generate economic return via personal income tax, VAT and local activity. With the motion approved in Congress, the debate is now unavoidable and Muñoz poses the three questions that now remain open: “Will the Government do it? When will it do it? How will it do it?”