A widow will have to return 6,877 euros to Social Security after compatible with the widowhood pension with the minimum vital income (IMV), which caused it to exceed the income limit required to collect this help. Although the woman communicated her new economic situation, social security took almost a year to extinguish the benefit, which caused this amount.

As explained by the sentence, this woman began to collect the minimum vital income in July 2020, at the same time that she had recognized the right to widow’s pension after her husband’s death in September 2019. The combination of both benefits caused 1020 to enter 10,704 euros, a figure higher than the income threshold set to access the IMV, which was 9,022 euros.

You may be interested

A woman runs out of the widow’s pension after living with her partner 24 years and grants the previous wife a pension of 1,663.87 euros: the de facto couple did not formalize

A woman achieves a pension of 2,071.29 euros by compatible retirement and widowhood after social security was removed for being incompatible: justice endorses

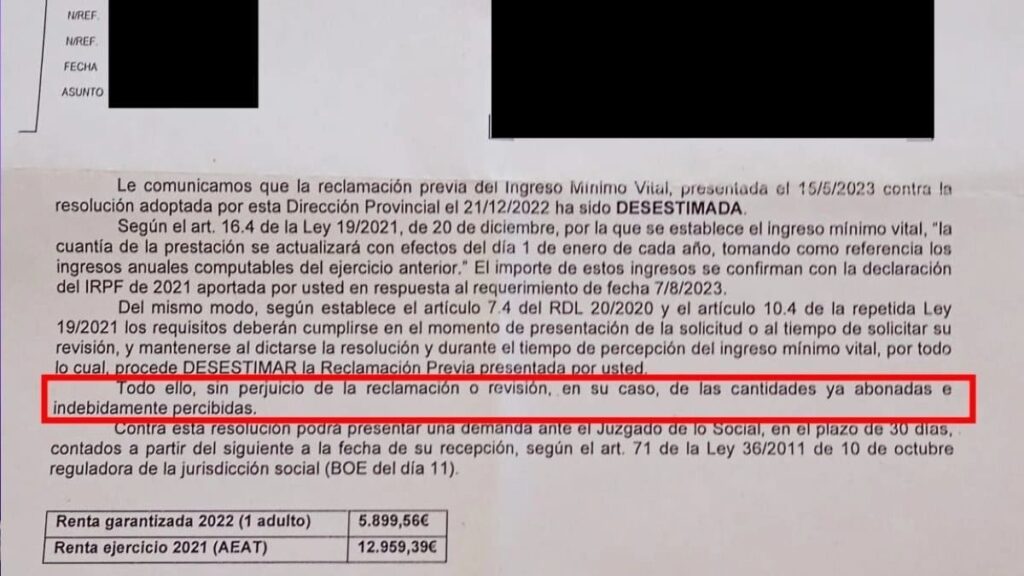

Almost a year later, Social Security verified the situation and realized that it no longer met the requirements to continue charging the IMV, so the benefit was extinguished since January of that same year. In addition, he was notified that he had to return 6,877.20 euros for unduly charged amounts between January and November 2021, as regulated by article 19 of Law 19/2021, of December 20 (it can be consulted in this Official State Gazette).

The widow did not be as she filed a claim to Social Security claiming that she always acted in good faith and that it was the INSS that took more than a year to review her economic situation. This was dismissed, so they decided to go to court.

In this way, both the Social Court No. 10 of Las Palmas de Gran Canaria and the Superior Court of Justice of the Canary Islands did not prove him right, when he understood that it was not an error of recognition of the benefit, but of an excess of income that made it incompatible with the IMV.

It was not a social security error

As the sentence details, the court explained that, although the widow acted in good faith and communicated to the Social Security that she was charging a widowhood pension, the obligation to return the minimum vital income leads directly from having overcome the threshold of income required to access the aid. That is, it does not question good faith and if the fact that overcome the income threshold demands return.

The Chamber acknowledged that Social Security took almost a year to extinguish the benefit after receiving the communication of the beneficiary, but clarified that this administrative delay cannot be considered an error in the recognition of the right, but a delay in declaring incompatibility. Therefore, the Cakarevic doctrine, of the European Court of Human Rights, which protects the beneficiaries when the improper collection is exclusively due to administration’s failures, that is, the return cannot be required if they are not blamed for the error, if they are not to blame for the error.

In this case, excess income was decisive and confirms the initial sentence, so the widow is obliged to reintegrate 6,877.20 euros unduly charged as IMV.