Source: https://www.imf.org/es

However, risks are increasing, particularly due to the concentration of investments in the technology sector and the negative effects of trade disruptions, which could worsen over time.

Global economic growth continues to show remarkable resilience, despite severe trade disruptions generated by the United States and increased uncertainty. According to our most recent projections, global growth this year will remain stable at 3.3%, an upward revision of 0.2 percentage points from October estimates, mainly attributable to the United States and China. It is worth noting that our current projections are almost unchanged from last year, as the global economy has managed to weather the immediate impact of the tariff shock.

This surprising strength reflects a confluence of factors, including easing trade tensions, higher-than-expected fiscal stimulus, accommodative financial conditions, the agility with which the private sector has managed to mitigate trade disruptions, and strengthening policy frameworks, particularly in emerging market economies.

Another key factor that has contributed to this resilience is the sustained increase in investment in the information technology sector, especially artificial intelligence. Although manufacturing activity remains subdued, investment in information technology as a proportion of US economic output has soared to its highest level since 2001, providing a notable boost to investment and business activity in general. While concentrated in the United States, this IT boom is also having positive impacts around the world, particularly in Asia’s technology export sector.

Financial conditions fuel growth

The rise in investment in information technology is a product of optimism among companies and markets about the transformative potential of recent technological innovations in the automation and artificial intelligence sectors and their promise to generate significant increases in productivity and profits. Since late 2022, when the first widely used generative artificial intelligence tools appeared, stock prices have seen a notable increase.

Favorable financial conditions and strong earnings have contributed to rising share prices and funded increased capital spending. However, with the acceleration of expansion, debt financing has become more frequent, and this has increased leverage. This shift poses significant risks: higher leverage could amplify shocks if profits fail to materialize or if financial conditions more broadly tighten, harming businesses and raising concerns about the impact on the financial system as a whole.

Additionally, profitability could be affected by assumptions surrounding payback schedules for advanced processors. The need to frequently upgrade equipment will reduce profit margins, eat into profits, and require a substantial increase in debt financing. These factors underscore the importance of monitoring rising leverage and its potential to exacerbate vulnerabilities.

The moral of dotcom

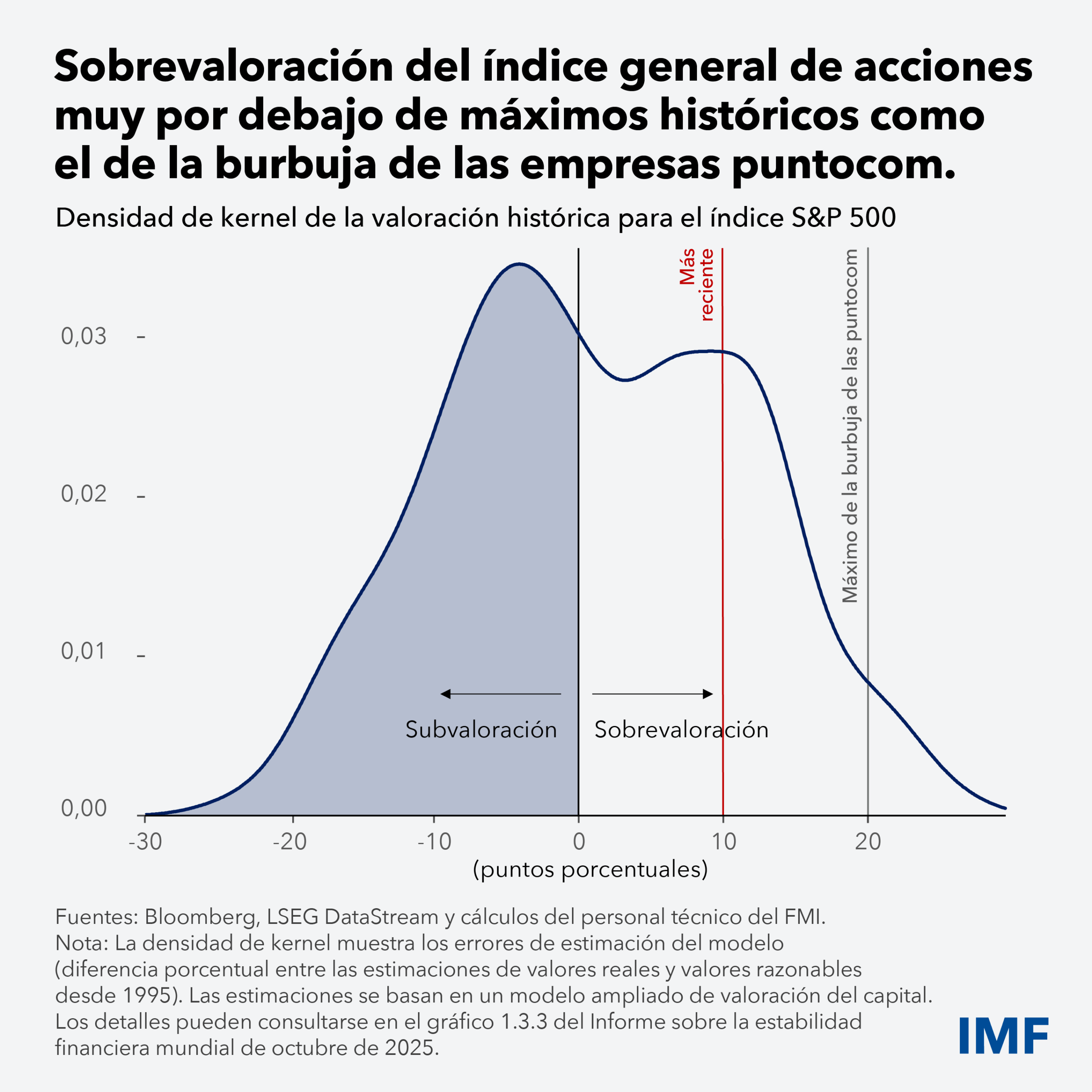

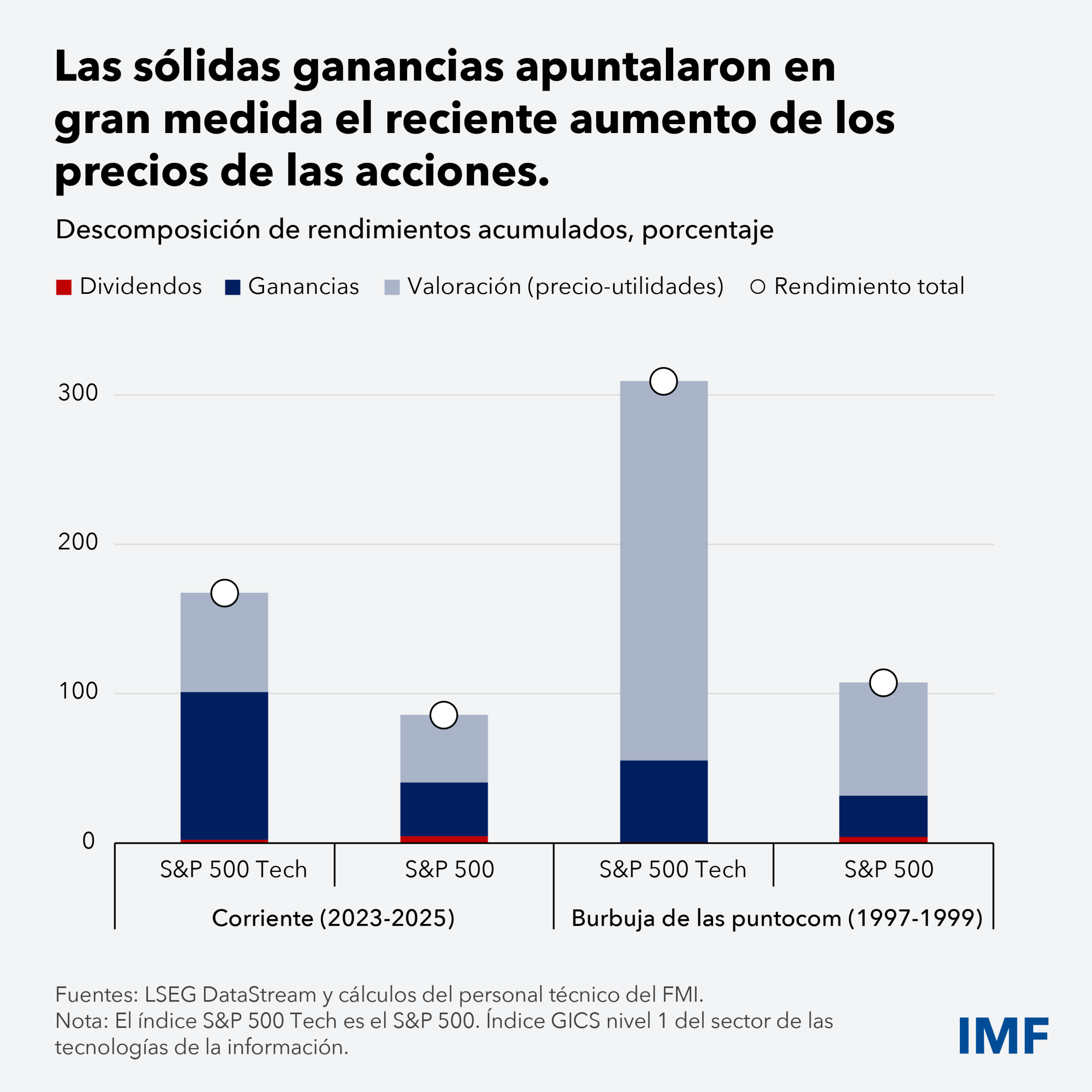

A comparison with the dot-com boom of 1995–2000 is sobering. Although investment in information technologies as a proportion of gross domestic product is generally similar to what it was then, the recent increase has been more gradual and accelerated only last year. Furthermore, although market valuations of the product have increased at a similar rate in both episodes, the increase in the price-earnings ratio has been more modest during the current boom because profits are higher.

In summary, our analysis suggests that the possible overvaluation of the general stock index in the United States is equivalent to barely half of that registered during the dotcom episode. However, there are three reasons why global macroeconomic growth could be highly vulnerable to a rally in technology stock prices.

First, the rise in stock prices in recent years has been driven primarily by the technology sector, particularly stocks related to artificial intelligence, and this small group has become one of the main pillars of the index. Secondly, many of the largest companies in the artificial intelligence sector are not yet listed on stock markets. Their level of debt could have consequences that were not seen during the dot-com era. Third, market capitalization relative to output—which in the United States rose from 132% in 2001 to 226% today—is now much higher, so even a slight correction could have profound effects on overall consumption.

Risks to the outlook

Looking ahead, the current boom in technology stocks poses considerable upside and downside risks to the global economy. On the positive side, promises of greater productivity thanks to artificial intelligence could begin to come true and push up activity in the United States and the world by 0.3% compared to the base case.

On the downside, AI companies may not deliver earnings commensurate with their lofty valuations, which could discourage investors. For reference, in an October 2025 World Economic Outlook scenario—which includes a slight correction to AI stock valuations and foresees a tightening of financial conditions—global growth declines by 0.4% relative to the base case. This could have far-reaching consequences if the decline in real investment in technology sectors becomes more pronounced and leads to costly reallocation of capital and labor. If the increase in total factor productivity is lower than forecasts and deeper corrections occur in stock markets, the losses in terms of world product could become even more accentuated, concentrating in regions with a strong technological profile, such as the United States and Asia.

Foreign ownership of U.S. stocks has been rising for a decade, so such a sharp correction could trigger large wealth losses outside the United States and weigh on consumption, spreading the slowdown to other regions of the world. Even economies with low exposure to technology, including many low-income and highly indebted countries, would be hit by negative spillovers on external demand and rising external borrowing costs.

These adverse factors arise at a time when, on the one hand, geopolitical uncertainty and the use of export controls on key inputs and other trade restrictions have increased, while on the other hand, many countries have seen their fiscal space erode. In this context, any revaluation of the increase in productivity induced by artificial intelligence or readjustment of the price of risk assets could generate an increasingly intense vicious circle.

Policies in favor of stability, discipline and inclusion

In a context of overvalued assets, increased debt financing and greater uncertainty, prudential supervision is essential to safeguard financial stability. Supervision and regulation should ensure that banking and non-banking institutions, particularly those exposed to the technology sector, apply strict loan underwriting standards. It is important to adhere to internationally agreed standards for bank capital and liquidity. Authorities must be ready to implement contingency plans to face various risks.

Monetary policy must find a delicate balance. If the tech boom continues, neutral real interest rates could rise—as they did during the dot-com era—requiring a tightening of monetary policy. This would reduce fiscal space, particularly in countries where artificial intelligence does not boost growth.

If the adverse scenario materializes, the rapid decline in aggregate demand will require a rapid reduction in monetary policy rates.

Properly diagnosing and calibrating monetary policy to achieve price stability requires central banks to operate within the confines of their mandate. The independence of central banks, which protects the credibility of monetary policy and allows inflation expectations to be anchored, is fundamental for monetary and financial stability and economic growth.

At the fiscal level, governments must redouble their efforts to reduce public debt and restore fiscal space where appropriate.

The uneven impact of artificial intelligence on workers is another important consideration. While innovation drives growth, there is a risk that jobs will disappear and wages will decline in certain segments of the labor market. Policies should focus on reducing barriers to adoption, helping workers invest in developing necessary skills, promoting labor mobility through targeted programs and ensuring competitive markets to facilitate entry and ensure that the benefits of innovation are widely disseminated.

In search of balance

The resilience of global growth to trade shocks has been extraordinary, but it masks underlying fragilities due to the concentration of investment in the technology sector. Furthermore, the negative effects of trade shocks on growth are likely to accumulate over time.

AI-related investments hold transformative potential, but they also pose financial and structural risks that require vigilance. The challenge for policymakers and investors is to balance optimism with caution and ensure that the current technological explosion translates into sustainable and inclusive growth and is not another cycle of boom and bust. This is especially important in a context characterized by worsening geopolitical tensions and growing threats to institutional frameworks that make the implementation of sound policies difficult.