The General Directorate of Taxes (DGT), dependent on the Ministry of Finance, has resolved a common doubt in income campaignCan parents apply the minimum for descendants in their declaration if their child has worked and decides to file personal income tax on their own? In its binding consultation V1445-25, dated July 29, 2025, it confirmed that yes, parents can apply the minimum for descendants in their personal income tax return even if their children file their own return, as long as certain income and cohabitation requirements are met.

The minimum for descendants adjusts the tax burden based on the personal and family circumstances of the taxpayer. It is regulated in article 58 of Law 35/2006, of November 28, on Personal Income Tax (LIRPF), and its purpose is to fiscally protect those who They have people in their charge.

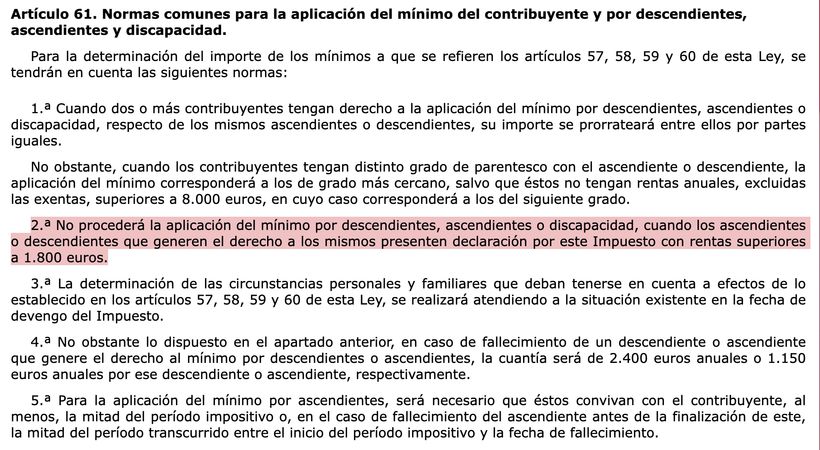

In order to apply it, the requirements of article 61 of the LIRPF must be met, which requires that the descendant:

- Be under 25 years of age as of December 31 of the year (or older with a disability).

- Live with the taxpayer or depend financially on him.

- Do not obtain income greater than 8,000 euros per year, excluding exempt income.

- Do not file a personal income tax return on your own with income greater than 1,800 euros.

When can it be applied if the child presents his own personal income tax?

In the case analyzed by the DGT, the consultant’s daughter, 20 years old, worked in the summer of 2023 obtaining 1,348 net euros of work performance. No withholding was applied to him, but he wanted to file his own return for personal reasons. The father asked if he could still apply the descendant minimum on his return.

The DGT clarified that what is relevant is not that the child presents a declaration, but whether or not it exceeds 1,800 euros of net income. In this sense, article 61.2 of the LIRPF establishes that the minimum for descendants may not be applied when the descendant submits an income tax return with income greater than 1,800 euros. It does not say that you are automatically excluded for presenting the income, but only if that threshold is exceeded.

Furthermore, the DGT recalled that to calculate this limit, the net income from work is taken into account, that is, income minus deductible expenses (according to article 19 of the LIRPF). In this case, the amount obtained did not exceed 1,800 euros and, therefore, the requirement is met even if the daughter presented her personal income tax.

Another of the fundamental elements is economic dependence or habitual coexistence. Although it is not required that the child physically live with the father at all times, the consultation clarified “that dependence on the latter will be assimilated to living with the taxpayer.”

The DGT confirmed that, under these conditions, the father can continue to apply the minimum per descendant of 2,400 euros to his personal income tax, since the presentation of an independent declaration for his daughter does not prevent him from doing so if he does not exceed the established limit.