The Treasury sends thousands of notifications to taxpayers every year, but not all of them have the same importance. Among them there is one that should not be overlooked, because not addressing it could end in a sanction. This is the request of the Tax Agency, an official communication in which the organization requests information, documentation or the appearance of the citizen for a matter with fiscal significance.

Article 203 of Law 58/2003, General Tax, states that resistance, obstruction, excuse or refusal to the actions of the Tax Administration constitutes a serious infraction. And this assumption expressly includes not responding to a duly notified request. That is to say, we cannot allege that “we did not know the rule”, since as article 6 of the Civil Code explains, “ignorance of the laws does not excuse compliance with them”; In other words, not knowing the rule does not excuse its mandatory compliance.

This means that, if the Treasury requests documents, data or the presence of the taxpayer and the taxpayer does not comply, the door may open to a fine. The amount will depend on the type of requirement, whether it has already been breached before and also whether the case occurs within an inspection procedure.

The law doesn’t just talk about not answering a letter. It also considers conduct such as not facilitating the examination of documents, books, invoices or computer files, not appearing when summoned without justified cause, preventing officials from entering a premises or even coercing them during the action, as an infraction.

Therefore, when a notification of this type arrives, the important thing is not only to open it, but to check exactly what the Tax Agency is requesting and within what period it must be attended to. In some cases, specific documentation will be requested. In others, the appearance of the taxpayer or access to certain accounting information.

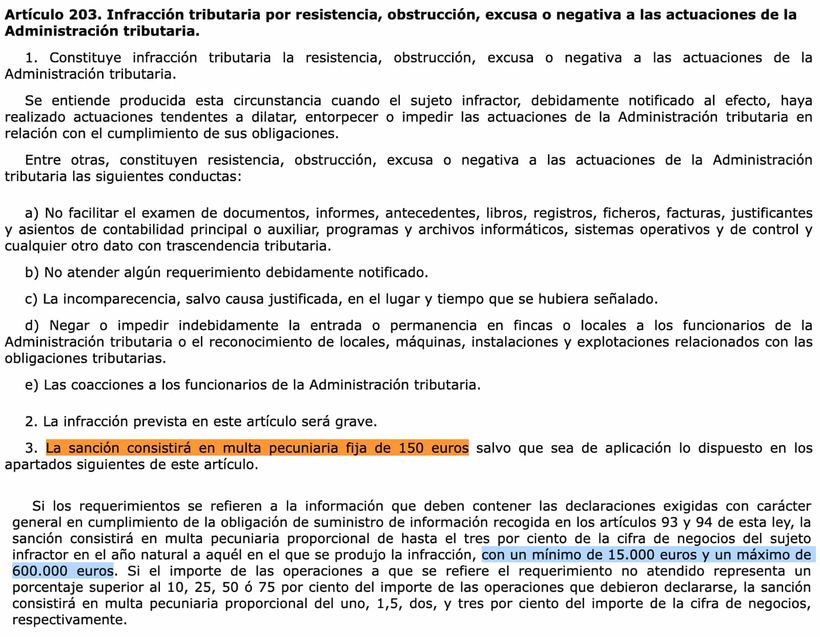

Fines of 150, 300 and 600 euros in the most common cases

The most common penalty for failing to comply with requirements starts at 150 euros when it is not complied with for the first time. If it happens a second time, the fine increases to 300 euros. And if a third breach occurs, it reaches 600 euros.

Now, the situation changes when what is not fulfilled affects accounting documentation, record books, files with tax significance or requirements addressed to businessmen and professionals within more complex actions. There the sanctions stop being merely fixed and begin to escalate much more harshly.

In these cases, the fine can start at 300 euros in the first request and 1,500 euros in the second. If non-compliance persists, the law allows imposing sanctions proportional to the turnover, with amounts that can vary between 10,000 and 400,000 euros, and even between 15,000 and 600,000 euros when it comes to particularly relevant reporting obligations.

When are the highest penalties reached?

Fines of up to 600,000 euros are not applied for not responding to any ordinary letter from the Treasury. They are provided for the most serious cases, especially when there is economic activity, an open inspection action and a repeated refusal to provide information, show accounting or allow access to essential documentation for tax verification.

Therefore, although many notifications may seem routine, it is worth reviewing them carefully. An ignored request can end up being much more expensive than it seems at first. In tax matters, missing deadlines is almost never a good idea.