By Santiago García-Mussons

Buy 100% using your portfolio as collateral: keep your investments working while you sign the mortgage.

Your investment portfolio remains as guarantee or guaranteeyou remain the owner and allow it to continue growing (compound interest).

This may mean tens of thousands of euros in your favor in a few years. I’ll show you below.

What happens when you DO NOT pledge:

You sell your portfolio (or part of it) to pay the down payment for a flat or a house.

- ❌ You pay taxes

- ❌ You are left without your investment portfolio

- ❌ You lose source of income

What happens when you DO pledge:

- ✅ Not for sale. You do not have to sell your investments, so you do not pay taxes on the capital gains generated at the time of purchasing the apartment.

- ✅ Assets can continue generating profitability: Your investments remain invested and can continue to generate profits (dividends, appreciation), which can potentially exceed the cost of the loan.

- ✅ Favorable loan conditions: By offering solid collateral, it is possible to obtain a loan with lower interest.

- ✅ You get both things: keep your wallet and buy an apartment.

Let’s look at an example to clearly see the advantages:

Buy 100% using your wallet as collateral

The bank lends you the 80% with normal mortgage and 20% extra with a loan cheaper because you leave your wallet as collateral. You do not sell your funds, ETF’s or shares: they remain reserved as a guarantee.

Example assumptions:

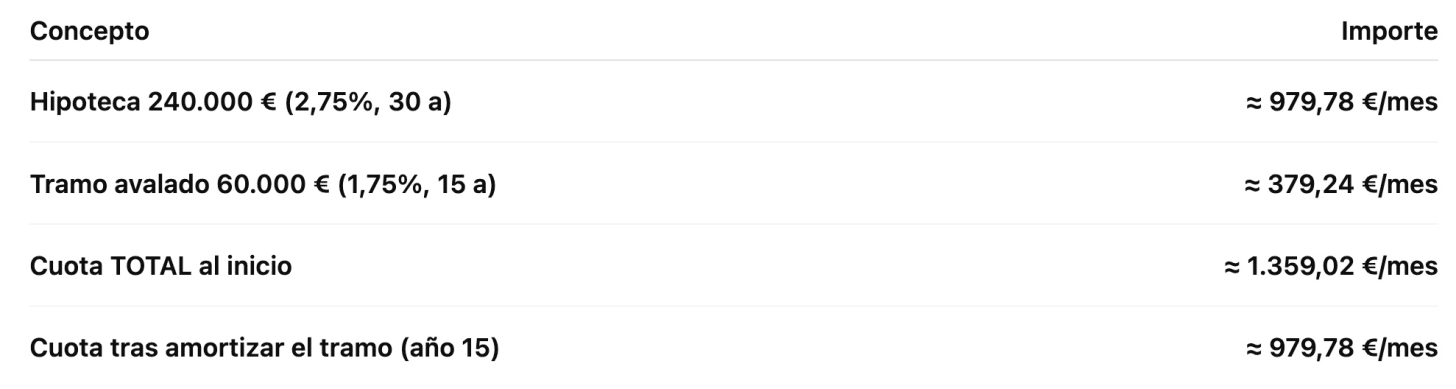

- Apartment price: €300,000

- Standard mortgage (80%): €240,000 a 2.75% TIN, 30 years

- Guaranteed section (20%): €60,000 to 1.75% TIN, 15 years

- Your portfolio today: €200,000 → you decide to give as collateral the 70% (= €140,000). This means that you will not be able to touch this €140k. You keep the rest to manage as you wish.

- The bank analyzes your 140k portfolio and accepts a 70% as a useful guarantee → €98,000 (enough to cover the €60,000 entrance with mattress)

- Portfolio profitability: +8% annually

- (Actual expenses/taxes and APR outside the example to focus the mechanics.)

1) How much do I pay per month?

With guarantee you pay more at the beginning (because the entrance section is going to 15 years), but you don’t sell the wallet and this keeps growing.

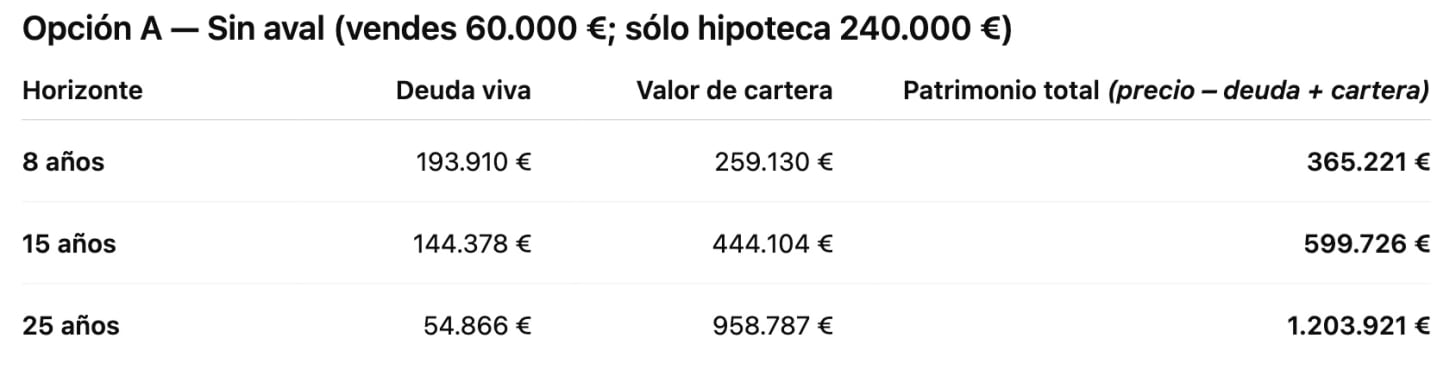

2) How will my assets look over time?

A) Unpledged (without endorsement, guarantee)

B) Pignoring (with endorsement, guarantee)

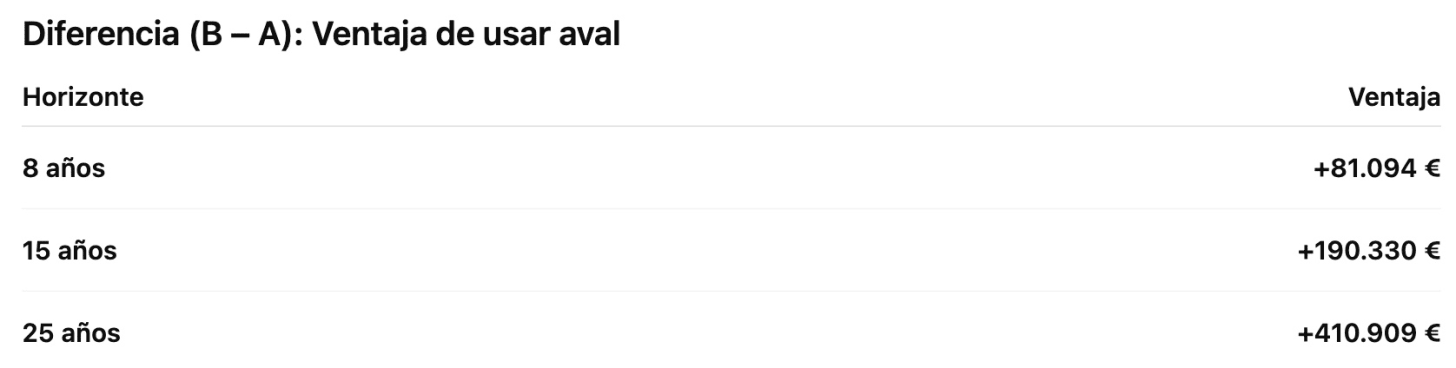

How much do you earn by pledging? 👇🏼

Why does he win? You don’t sell the €60,000which grow at +8%, and the guaranteed tranche is cheap and fast (15 years). You pay more fee at the beginning, but you heritage rises much more in the medium term.

Summary

If your portfolio yields more than its real cost and you can assume the initial payment, using it as collateral for 20% allows you to buy 100% without “killing” the compound interest, always with some safety margins.

Things to keep in mind:

- The bank does not take your wallet 100%: applies a discount.

- If your portfolio counts 70%, As the example, €100,000 goes to €70,000 guarantee.”

- With sufficient guarantees, you can go from 70% to 90–100% financing. But If the market falls, they may ask you for more guarantees: that’s why you need mattress and a portfolio of quality.

Here I leave you indicative percentages:

- 90-100% if you have it in cash or monetary.

- 70-90% if you have it in “investment grade” and short-term fixed income.

- 50-80% if you have it in global equity funds and ETFs.

- 20-60% if you have it in actions.

- 0% if you have it in cryptos and illiquid assets.

Risks to consider:

- APR vs TIN: look at the APR (includes commissions/insurance), not just the nominal rate.

- If the value of your portfolio drops significantly, the bank could request additional collateral or foreclose (sell) your pledged assets to cover the debt, often at an inopportune market time. Importance of mattress.

- The pledged assets are “locked” and you cannot freely dispose of them or use them for other operations for the duration of the loan.

- You are using debt to finance the purchase, which increases your financial exposure and the overall risk to your equity. Importance of mattress.

In summary…

If your wallet yield more than the actual cost of your mortgage, use it as collateral allows you not sell and maintain compound interest.

The key is the discipline: mattress, portfolio quality and understanding how the endorsement (discounts and possible calls if the market falls).

Don’t sell your engine of wealth to start the car. Use it as collateral.

I hope it has helped you learn about this method for financing the purchase of an apartment and that you found it interesting.

See you next week and, if you want to invest in the fund Top Quality OpportunitiesI leave you the next point.

Invest in Top Quality Opportunities

You already know that investing in the Top Quality Opportunities fund is available to everyone.

✅ You have it available in MyInvestor, Andbank and Creand (Andorra and Spain).

- ISIN: ES0131444145

- Minimum Investment: 10 euros.

- Open an account in MyInvestor and receive €25

- More information