Spain’s public pension system has faced major reforms (Law 27/2011, Law 21/2021 or Royal Decree 2/2023) with the aim of creating and guaranteeing the public Social Security pension system. But, while seeking to protect the purchasing power of retirees by increasing contributions and budget transfers, a comparative analysis of the pension models of Sweden, Chile and Germany shows a key fact and that is that the Spanish system is a financial anomaly in its environment.

The report Comparative Pension Systems, published by the Ruth Richardson Center of the University of the Hesperides, warns that the lack of automatic adjustment mechanisms condemns Spain to unprecedented fiscal pressure. The study launches explains that without a structural reform that introduces automatic rules, as Sweden or Germany have done, or capitalization elements, as in Chile, “the current model is financially unsustainable” and spending will skyrocket by 3.6 points of GDP between now and 2070.

You may be interested

Elma Saiz sees an increase of more than 5% in non-contributory pensions as “reasonable”

Oswaldo Martín (75 years old), retired with a pension of 900 euros per month: “I worked for 22 years from 12:30 at night to 12 noon for 1,500 euros”

Economists Daniel Fernández, Santiago Calvo and Miguel González, authors of the document, contrast the rigidity of Spain’s pay-as-you-go model with the flexibility of the reforms undertaken by these three countries. The most eloquent data provided by the report is that of the pressure on the active population, where the average public pension in Spain is equivalent to 66.4% of GDP per capita, the highest level in the sample, compared to 45.9% in Germany, 39.2% in Sweden or 28.7% in Chile. This relative generosity, they warn, is based on a growing debt (105% of GDP in Spain compared to 36% in Sweden) that mortgages future generations.

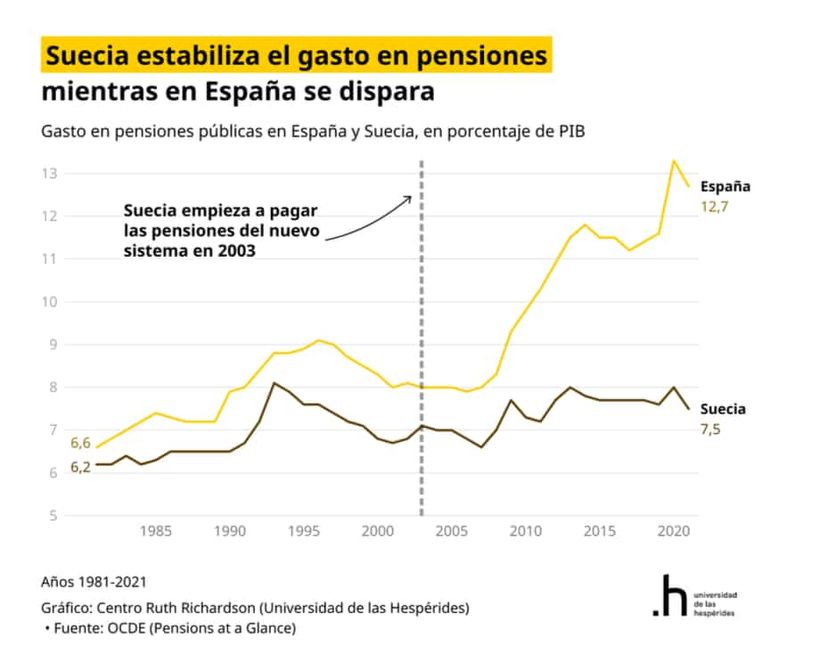

Sweden appears in the analysis as the mirror in which Spain should look at itself to avoid the bankruptcy of the system. After the crisis of the 1990s, Stockholm abandoned political promises to embrace financial mathematics. The Nordic country implemented so-called notional defined contribution accounts (NDC), a system where each worker accumulates real pension rights in a virtual account, automatically adjusted by life expectancy and economic growth.

The key to Swedish success, according to the report, lies in its “automatic brake”, that is, if the system’s liabilities exceed assets, pensions are adjusted downwards without the need for a parliamentary vote, thus depoliticizing sustainability. Furthermore, transparency is absolute, since the citizen annually receives an “orange envelope” with the exact situation of their savings, which aligns the expectations of the population with the economic reality of the country. The result is that Sweden has managed to stabilize its spending on pensions at 7.5% of GDP, while Spain already dedicates 12.7%.

The Chilean model and asset accumulation

The study also dismantles prejudices about the Chilean system, a pioneer in mandatory individual capitalization since 1981. Although criticized for its lower replacement rates (36% compared to 86% in Spain for medium incomes), the report highlights its macroeconomic solvency. By making each worker the owner of their savings through accounts managed by private entities (AFP), Chile has accumulated financial assets worth 75.8% of its GDP, compared to Spain’s meager 10.5%.

This huge mass of savings not only protects future pensions from demographics, but has also boosted the capital market and the country’s growth. Furthermore, the model encourages activity: 20.2% of those over 65 years of age in Chile continue to work, compared to 3.6% in Spain, which raises their total income (adding pension and salaries) to 93.5% of the national average, even exceeding the OECD average.

Germany and the cost of not thoroughly reforming

Finally, the case of Germany serves as a warning about half-solutions. Berlin, with an aging problem similar to that of Spain, has chosen to protect by law the replacement rate at 48% of the average salary. However, the report warns that this measure has a high cost: it will require raising contributions from the current 18.6% to 22.3% and increasing federal subsidies, which already cover a quarter of pension spending.

Although Germany has created the Generationenkapital (a sovereign fund to invest in capital markets), the authors consider that its scale is insufficient to compensate for the deficit of the pay-as-you-go system.

The final message for Spain is that to guarantee the sufficiency of pensions without suffocating active workers, it is imperative to diversify sources of income in old age (promoting corporate and private savings) and introduce automatic rules that adapt the system to demographic reality, instead of legislating with our backs to it.