Early retirement allows workers to leave working life before their ordinary age, but knowing that Social Security will apply a “penalty”, which are cuts in the form of a percentage, which will depend on the modality (voluntary or involuntary), the total years of contributions and the months advanced with respect to the ordinary age.

Within the system, voluntary early retirements allow a maximum advance of two years. For this reason and if we look at Law 27/2011, which regulates the ordinary retirement age, it is possible to retire at 63 years of age, although it is necessary to meet a series of requirements.

To begin with and according to article 208 of the General Law of Social Security (You can check it out at this link) it is necessary not only to prove a minimum of 35 years of contributions throughout your working life, which is what the LGSS imposes, but it is also essential to have 38 years and three months of contributions, since those are the years of contributions necessary to retire at age 65 and, thus, be able to advance your age by 2 years (24 months), which is the maximum.

In addition to the total number of years worked, at least two of these must be included within the 15 years immediately preceding the moment the right arose (what is known as the “causing event”). To obtain all these contributions, Social Security allows computing the period of compulsory military service, substitute social benefit or compulsory female social service, with a maximum limit of one year.

The amount of voluntary early retirement must be higher than the minimum pension

To retire early voluntarily, it is necessary that the amount of pension received is greater than the minimum that would correspond to the pensioner, depending on his or her family situation, upon reaching 65 years of age. If the calculation after applying the reducing coefficients is less than that minimum, Social Security will deny it.

According to Royal Decree 3/2026, the minimum annual retirement amounts for 2026 are the following:

| Retirement pension | With dependent spouse (€/year) | Without spouse: Single-person economic unit (€/year) | With non-dependent spouse (€/year) |

|---|---|---|---|

| Owner 65 years old | €17,592.40 | €13,106.80 | €12,441.80 |

| Owner under 65 years of age | €17,592.40 | €12,262.60 | €11,590.60 |

| Owner aged 65 with severe disability | €26,385.80 | €19,660.20 | €18,662.00 |

The minimum monthly amounts are the following:

| Retirement Pension | With dependent spouse (€/year) | Without spouse: Single-person economic unit (€/year) | With non-dependent spouse (€/year) |

|---|---|---|---|

| Owner 65 years old | €1,256.6 | €936.2 | €888.7 |

| Owner under 65 years of age | €1,256.6 | €875.9 | €827.9 |

| Owner aged 65 with severe disability | €1,884.7 | €1,404.3 | €1,333 |

Cuts in the voluntary early retirement pension

As occurs in the involuntary modality, in voluntary early retirement, Social Security applies a cut in the pension to compensate for the early retirement and the premature cessation of contributions to the system. That is to say, since we enjoyed the subsidy before and it is understood that it will be collected for a longer period of time, the amount should be reduced.

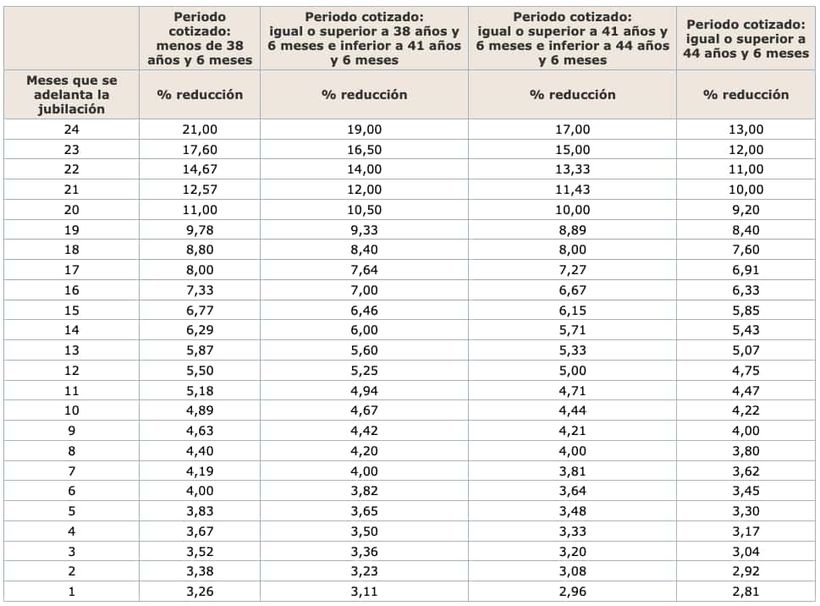

These cuts are implemented through monthly reducing coefficients that are applied to the amount of the pension once calculated. Unlike the involuntary option, this modality allows a maximum advance of two years (24 months) with respect to the ordinary age. The penalty percentages vary depending on the advance time and the total period contributed by the worker:

- For workers with less than 38 years and six months of contributions: the cut is 21% if they retire with a maximum advance of two years, and 5.50% if they only advance their retirement one year.

- For workers between 38 years and six months and 41 years and six months of contributions: the reduction is 19% for two years of advance and 5.25% for one year.

- For workers between 41 years and six months and 44 years and six months of contributions: the cut percentage is 17% if they retire two years in advance and 5% if they retire one year in advance.

- For workers with more than 44 years and six months of contributions: the penalty is the lowest, standing at 13% for two years in advance and 4.75% for one year in advance.

What happens if the worker has a very high regulatory base? If after applying the cuts, the resulting pension is still higher than the maximum legal limit, a specific adjustment is applied. In accordance with Royal Decree-Law 3/2026 and included in article 210.3 of the law, the reducing coefficients that correspond by age will be applied directly to the limit of the maximum amount of pensions.

For this year 2026, this maximum amount is set at 3,359.60 euros per month (47,034.40 euros per year), as established in the revaluation regulations and budgets for this year.