The Tax Agency allows you to view the tax data of taxpayers for the 2025 financial year from March 18, 2026, before the Income Tax return campaign begins. This document is a summary of all the information that the Treasury already has about the taxpayer, that is, income from work, bank interest, real estate, capital gains and deductions of which the AEAT is aware.

It is advisable to review before confirming the draft, since errors can be avoided that could lead to a complementary assessment or the loss of deductions that the taxpayer was entitled to apply. What’s more, it can cause a declaration to pay less or even cause the Treasury to have to return more money.

Where to consult tax data

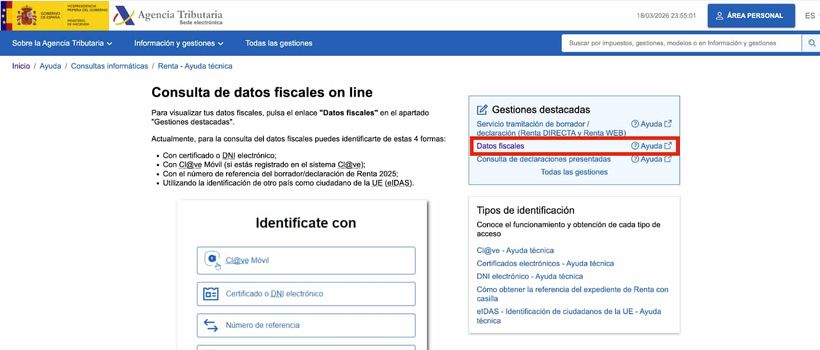

The tax data is available on the electronic headquarters of the AEAT (sede.agenciatributaria.gob.es), which is the main channel. It is accessed from the Personal Income Tax section, within the “My files and tax data” section, and from there you can also download the document in PDF. Those who prefer to do it from their mobile phone can use the official AEAT app, available for iOS and Android, which works with the same identification systems as the headquarters.

What do you need to identify yourself?

To access tax data, the Tax Agency accepts four identification systems:

- Digital certificate: issued by the National Mint and Stamp Factory or another recognized certification entity.

- Electronic DNI: the national identity document with an active chip and a card reader.

- Cl@ve: the Government identification system that works with a username and password or with a single-use PIN sent to the mobile phone.

- Reference number: obtained by combining the NIF, the expiration date of the DNI or the date of birth if you are the holder of a NIE, and box 505 of the last declaration submitted. Those who did not file a return the previous year can request the reference number with the IBAN of a bank account they own.

What information does the tax data contain?

The document brings together the information that the AEAT has received from companies, financial entities and public organizations during the 2025 financial year:

- Work income: gross amount received from each payer, withholdings made and Social Security contributions.

- Income from movable capital: interest from bank accounts, dividends and other financial income, with their withholdings.

- Capital gains and losses: transfers of real estate, investment funds and other assets reported to the AEAT.

- Real estate capital returns: rents received, when the tenant is a company or entity required to report.

- Property data: cadastral reference, cadastral value and location of the properties of which the taxpayer is the owner.

- Deductions: contributions to pension plans, donations to non-profit entities and other deductions of which the AEAT is aware.

Why they are not always complete

Fiscal data is the starting point of the draft, but it is not always complete. Self-employed workers who invoice individuals may find that their income is not reflected, because individuals do not have the obligation to inform the AEAT of their payments, unlike companies, which must submit form 190. The same occurs with rents collected from a private tenant, if the tenant is a natural person, the income does not appear automatically. Profits not reported to the AEAT also do not usually appear, such as sales between individuals, cryptocurrencies not held in custody on Spanish platforms or other assets without obligation to report. Regional deductions, for their part, do not always appear preloaded in the draft and must be added by hand.

There is a different case that does appear in the 2025 tax data and it is the income obtained on digital platforms such as Airbnb, Wallapop, Vinted or Uber. Since 2023, these platforms are required by the European DAC7 Directive to report the income of their users to the tax authorities. Anyone who has rented a room, sold second-hand items or provided services through these applications can find these amounts already incorporated into their tax data.

Confirming the draft without reviewing these situations is equivalent to submitting an incomplete declaration. If the result is a refund greater than what would be appropriate or an income lower than the correct amount, the Tax Agency may issue a complementary settlement with a surcharge of between 5% and 20% according to article 27 of the General Tax Law (consultable in this BOE).