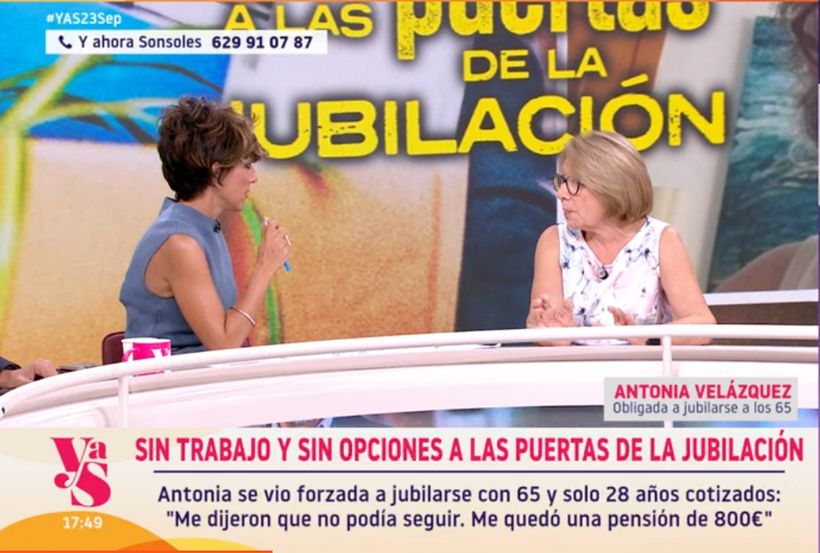

Antonia, a worker who began her career at the age of 14, today faces a retirement of just 800 euros per month after being forced to retire when she reaches the legal age. Despite having worked for more than five decades in sectors such as hospitality or care, she only has 28 years of official contributions, since she was not registered with Social Security until she was 43 years old.

His case illustrates the vulnerability of thousands of pensioners in Spain who, due to the shadow economy of the past and current sustainability rules, receive benefits that are 46% below the average pension, which in this month of April alone, rises to 1,485 euros.

Architects agree: “never paint your bedroom white”

A Google editor reveals the three questions we ask most when no one sees us: “we are losing our basic life skills”

The late quote

The public pension system in Spain is experiencing a paradox: while monthly spending already exceeds 13.5 billion euros, the “rules of the game” leave out those who had long but administratively incomplete careers. Antonia relates that, despite her desire to remain active to improve her income, the company took advantage of its legal authority to terminate the contract: “They tell me that I have to retire at 65 years and 7 months (…) I tell them if I could continue working and they tell me no,” she laments during her speech in And now Sonsoles.

Antonia’s problem was not a lack of effort, but the absence of vacations and work rights for almost 30 years. “At the age of 43 I had my first vacation,” he confesses, pointing out that until that age he worked informally in bars, hairdressers and private homes, periods that the current system does not recognize for the calculation of the regulatory base.

What the data says

Expert analysts warn that the current reform of the system, which includes the Intergenerational Equity Mechanism (MEI) with a 1.2% tax, is designed to guarantee the survival of the fund before the retirement of the Baby Boombut not to compensate for historical injustices. In the current scenario, the last years of working life are decisive:

- Dual system: The last 25 or 29 years of contributions are chosen. If these last years were of low salaries, the pension plummets.

- Contribution gaps: Gaps without contributions drastically lower the arithmetic average of the benefit.

- Power of the company: Upon reaching the ordinary age, it is the employer’s power to decide whether to support the worker, preventing people like Antonia from continuing to contribute to increase their income.

The future of low pensions

For cases like Antonia’s, the only safety net is non-contributory pensions, although experts point out that these do not solve the structural problem. The system’s tendency is towards “paying fewer pensions” through reducing coefficients and stricter year requirements, instead of reinforcing the benefits of those who were victims of job insecurity decades ago.

Antonia’s situation puts a face to the 13% of GDP that Spain dedicates to pensions, reminding us that having a life dedicated to work does not always guarantee an old age with economic dignity in the current legal framework.