Economist Gonzalo Bernardos is clear: “Those who have a variable mortgage and the loan has more than 10 years left to repay it, take and change their mortgage,” he explains in Better LateLa Sexta program.

His message is aimed at those who are still in the most expensive part of the loan, when most of the payment is interest. “In mortgage wholesalers, in brokers digital, you can still find fixed rate mortgages at 2.4%,” adds the specialist.

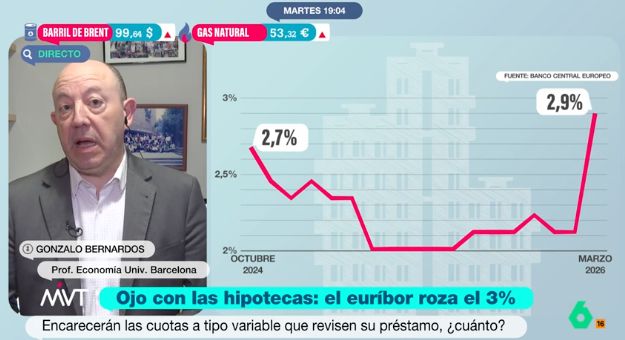

restless Euribor

Context helps understand his warning. After two years of respite from the peaks in 2023 and 2024, the Euribor has hit a considerable slowdown. In February of this year alone, it was found around 2.22% and the provisional data for March already place it between 2.4% and 2.5%, with days in which it even touches 3% in daily rate. All this in an environment marked by instability in the Middle East and the fear that energy inflation will tighten again.

For their part, Spanish banking analysts predict a relatively stable scenario for the end of the year with a Euribor between 2.25% and 2.30% if there is no geopolitical worsening.

But this ‘calm’ cannot be translated into those with variable rate mortgages being able to relax. If the oil war becomes complicated, rates may rise earlier and more than expected. And that is where Bernardos’ advice gains important weight: take advantage of the fact that there are still fixed or mixed offers around 2.4% to shield the monthly bill.

What happens when there are more than 10 years left to pay?

During his television intervention, the economist focused on a very specific group: those who have more than a decade of mortgage ahead of them. According to the French system, the most common in Spain, interest is paid during the first half of the loan and only a small part amortizes capital. In that section, every half point more of Euribor is very noticeable in the quota.

To get an idea, just look at the average. In 2026, the average new mortgage is around 165,000 euros for about 20 years. With a variable rate of around 3.2%-3.5% (adding Euribor and differential), the fee moves close to 950-1,000 euros per month.

If rates give an additional push, that figure could rise by tens of euros per month. On the other hand, moving to a fixed rate or a mixed rate with a fixed tranche at 2.4%-$1.8 reduces the risk of future scares. It is precisely this window of opportunity that Bernardos appeals to.

“The European Central Bank almost always screws up”

The economist does not stop at the figures alone: “When there is an oil crisis there is more inflation and when there is more inflation the European Central Bank should raise interest rates,” he recalls.

However, she assures that this entity “almost always annoys her.” His example: in 2022, inflation was already 5.1% in January, “excessive”, and it skyrocketed with the invasion of Ukraine, but the ECB kept rates at 0% and continued injecting liquidity until July.

Now, he warns, the official discourse is that they have “learned from their mistakes” and that, if the war drags on, they will move sooner. Translated into floor and mortgage language: if the conflict becomes entrenched, rates are likely to rise again faster than many households expect.

Safety net for the most suffocated

For those who already feel that the quota has become a burden, the system offers some escape valves. The so-called Code of Good Practices remains in force for households with modest incomes, around 33,000-37,800 euros per year, and allows negotiating with the bank measures such as freezing the installment for one year, extending the term of the loan up to seven more years (with the consequent decrease in the bill) or converting a variable mortgage into a fixed one without paying commissions.

Furthermore, if the mortgage eats up more than 50% of the family’s income, it falls into the category of special vulnerability, which opens the door to periods of capital deficiency, in which only interest is paid for a time.